(This is an excerpt from an article I originally published on Seeking Alpha on July 24, 2015. Click here to read the entire piece.)

{snip}

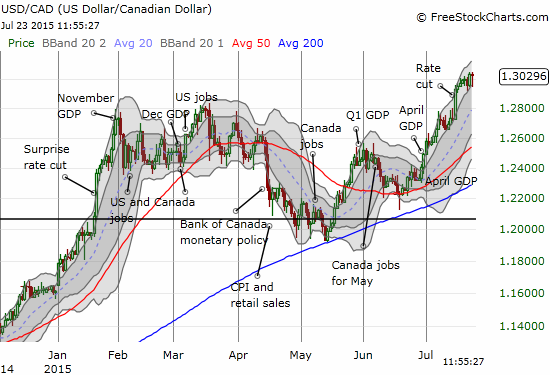

In the middle of this fresh decline, the Bank of Canada delivered its July Monetary Policy Report with another rate cut included. The reaction in the currency market was just as dramatic as the January rate cut. This time the Canadian dollar (FXC) hit levels last seen at the height of the financial crisis.

Source for charts: FreeStockCharts.com

The latest surge in USD/CAD is effectively a continuation of a net bounce off the 50-day moving average (DMA). I did not interpret this firm support as bearish for the Canadian dollar because at the time I assumed oil would at worst remain in a tight trading range. Even as I began to transition my trading bias on oil to bearish, I did not even consider another rate cut as a real enough possibility from the Bank of Canada. This blind spot was a result of my commitment to a longer-term bullishness on Canada, its economy, and its currency; I described my change from bearishness to bullishness in several pieces this year. The headwinds blasting at this bullishness remind me why in almost all cases I prefer to trade currencies with a short leash!

After reviewing the Monetary Policy Report (MPR), reading the opening statement of Governor Stephen S. Poloz, and watching the subsequent press conference, I have concluded that the Bank of Canada’s rate cut served very little purpose beyond confirming that the Bank is afraid economic conditions in Canada are at risk of getting much worse before they improve. The Bank is leaning ever more heavily on leveraging its exchange rate to push exports of non-energy related products into catalyst for GDP growth.

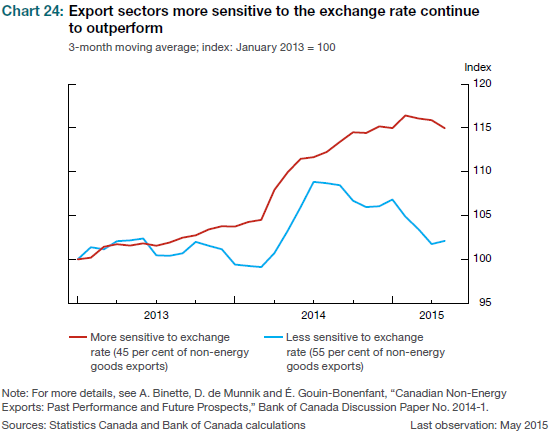

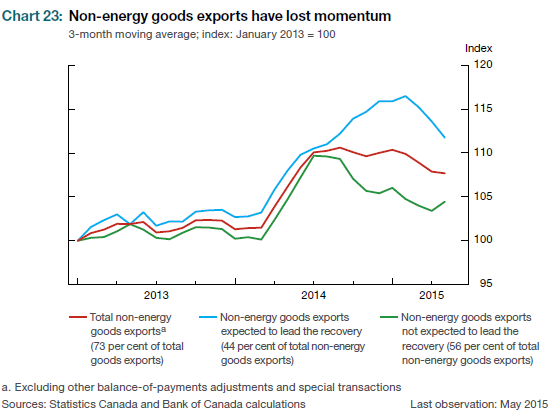

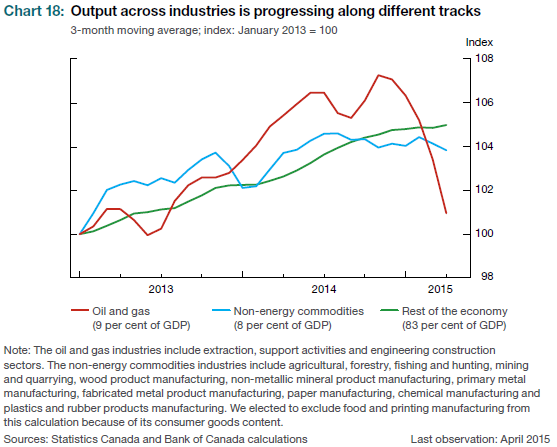

Three charts from the MPR that essentially tell the entire story for me.

{snip}

Source: Bank of Canada Monetary Policy Report, July, 2015

{snip}

Source: Bank of Canada Monetary Policy Report, July, 2015

{snip}

The dynamics shown in the above charts suggest to me that the Canadian dollar likely DOES need to get even weaker for Canada’s economy to regain its footing. The rate cut last week is a step toward achieving that goal.

Even more unsettling – the Bank is at a loss trying to explain the unexpectedly poor performance of exports and yet feels very comfortable cutting rates. I now wonder aloud whether the Bank has already accepted a very real possibility that quantitative easing is in its future?!?

{snip}

Poloz was not able to credibly explain how else the Canadian economy will benefit from a cut from 0.75% to 0.50% when the housing market in Canada’s largest cities are already booming and households are facing precarious debt imbalances. {snip}

{snip}

The rate cut HAS firmly planted Canada on the other side of the fence in a global economic story increasingly defined by policy divergence. {snip}

It is indeed all about the U.S.: “Over the remainder of 2015 and through 2016–17, Canadian exports should benefit from the growing strength of Canada’s major trading partner, the United States.”

{snip}

Source: Bank of Canada Monetary Policy Report, July, 2015

{snip}

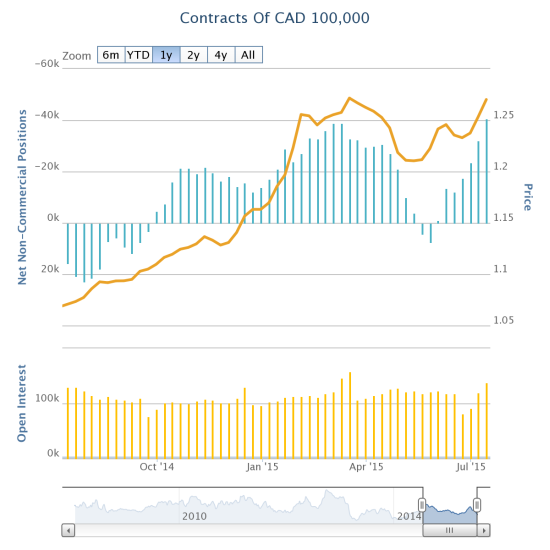

Source: Oanda’s CFTC’s Commitments of Traders

So at some point soon, I will lick the wounds, cut the losses, and reposition. The timing will depend on how the current collapse in commodities plays out. My sense is that the selling has become over-extended. In particular, I want to wait to see what happens if (when?) oil retests its recent lows. Stay tuned!

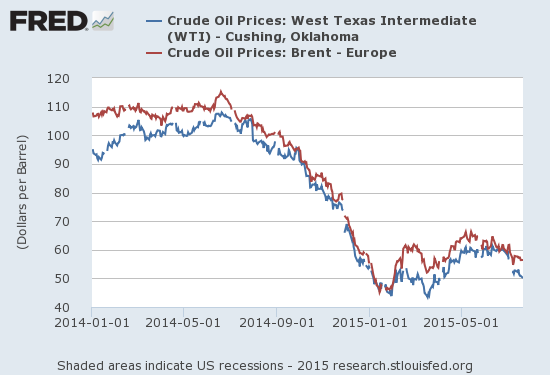

Source: US. Energy Information Administration, Crude Oil Prices: West Texas Intermediate (WTI) – Cushing, Oklahoma [DCOILWTICO], retrieved from FRED, Federal Reserve Bank of St. Louis, July 23, 2015.

US. Energy Information Administration, Crude Oil Prices: Brent – Europe [DCOILBRENTEU], retrieved from FRED, Federal Reserve Bank of St. Louis, July 23, 2015.

Be careful out there!

Full disclosure: long FXC, short USD/CAD

(This is an excerpt from an article I originally published on Seeking Alpha on July 24, 2015. Click here to read the entire piece.)