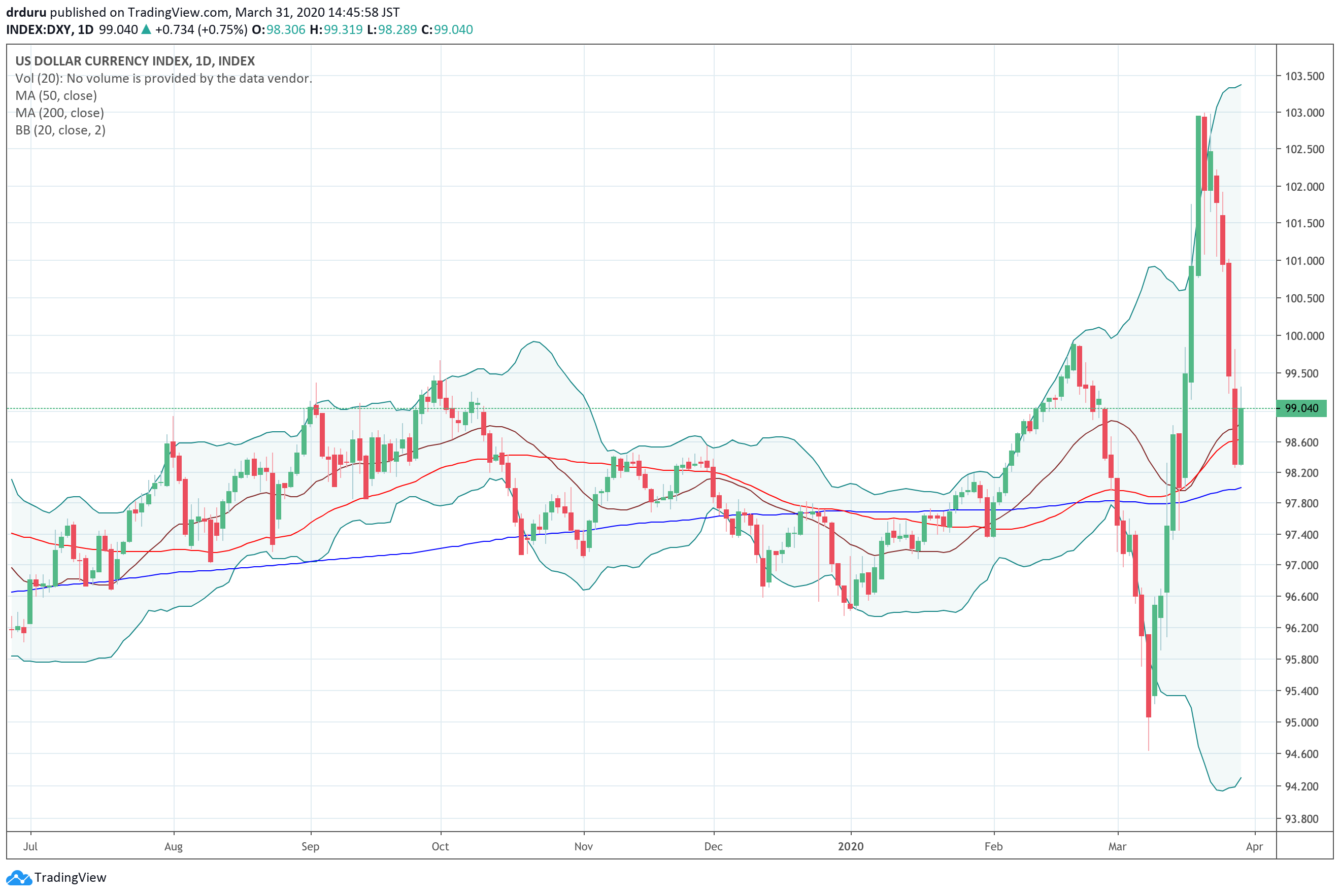

When the stock market sell-off began in earnest in late February, the U.S. dollar index (DXY) surprisingly plunged along with the major indices. I accepted the narrative explaining that the dollar’s decline came from the euro’s gain as “risk-off” traders rushed to close out euro shorts in carry trades. The swiftness of the risk-off move was a prelude to subsequent collapses in the stock market.

On March 10th, the steep slide in the U.S. dollar suddenly ended. The U.S. dollar index rebounded nearly 8 straight days to hit a new 39-month high. Once again, the end of the move came swiftly. On Monday (March 30th), the slide finally ended with what looks like the successful test of support at the 200-day moving average (DMA). This support was missing when the index sliced right through its 200DMA on March 2nd.

Source: TradingView.com

I cannot well correlate the dollar’s moves with the slew of emergency measures and announcements from the Federal Reserve. For example, on Sunday, March 15th the Federal Reserve coordinated with the Bank of Canada (BoC), the Bank of England (BoE), the Bank of Japan (BoJ), the European Central Bank (ECB), and the Swiss National Bank (SNB) to provide more liquidity in the U.S. dollar. The next day, the U.S. dollar pulled back slightly but resumed its steep rally for another three trading days. For a brief moment, financial markets had higher priorities than paying attention to that massive display of force in the currency markets.

The subsequent topping in the U.S. dollar corresponded with the current bottom in the S&P 500 (SPY). Opportunistically focusing just on this correlation, the market’s risk-on behavior took pressure of a fresh rush for the U.S. dollar and/or dollar-denominated assets.

Now with the dollar index apparently rebounding off 200DMA support, I find it useful to take a step back and look at the net movement in the U.S. dollar. The big moves are distracting from the simple fact that the dollar remains well supported by its 200DMA, even its 50DMA. The index is pivoting around these trendlines. I want to bet that this overall trend continues. I currently have a mix of short and long U.S. dollar currency pairs, but going forward I want to align more closely to the presumed trendline pivot.

Specifically, when/if the index moves “far away” from these trendlines, I will bet on a move in the other direction. Since I am long-term bearish on the euro, I will go short EUR/USD when DXY drops well below its 200DMA. I also like going long USD/JPY. When DXY soars well above its 200DMA, I will switch to long GBP/USD or even long AUD/USD. If the stock market is also in turmoil, I will favor a short USD/JPY position.

I will maintain this “pivot strategy” until/unless the U.S. dollar index breaks through the recent trough and peak of its wild swings over the past month.

Federal Reserve Unreserved

Speaking of the Federal Reserve, I almost missed Chair Jerome Powell’s appearance on the Today Show on March 26th (the Federal Reserve website posted a link to the interview). Powell clearly appeared in front of the American people to instill confidence and to explain the Fed’s emergency actions in simple and direct terms. We may one day look back and see this moment as critical to helping create a bottom (approximate?) in financial markets even as the coronavirus pandemic and resulting financial crisis continues to unfold.

Powell’s interview flashed me back to former Chair Ben Bernanke’s appearance on 60 Minutes on March 10th, 2009….two days after the S&P 500’s historic bottom.

Be careful out there!

Full disclosure: long SSO, long and short U.S. dollar currency pairs