The Bank of Canada changed its tune from the its last pronouncement on monetary policy. At that time, the Bank was very confident about the Canadian economy even as it mapped out the downside risks of the U.S. vs China Trade War. The Trade War remains unresolved three months later, and the Bank of Canada decided to downgrade its outlook while leaving rates unchanged. From the statement:

“The outlook for the global economy has weakened further since the Bank’s July Monetary Policy Report (MPR). Ongoing trade conflicts and uncertainty are restraining business investment, trade, and global growth.”

The kicker was the Bank of Canada’s downgrade of economic growth. For 2019, the Bank of Canada went from 1.3% real GDP growth to 1.5% (which is still a “a rate below [the economy’s] potential”, BUT growth for 2020 went from 2.0% to 1.7%. Growth for 2021 went from 2.0% to 1.8%. The statement also noted that “…the resilience of Canada’s economy will be increasingly tested as trade conflicts and uncertainty persist.” During the press conference, Bank of Canada governor Stephen S. Poloz referred to economic “shocks” and worsening trade risks.

Poloz provided more details about the risks and deterioration in his opening statement at the press conference (emphasis mine):

“Not surprisingly, the worsening global situation was the primary issue. Economic forecasts have been marked down further in most countries, largely as a consequence of the escalation of trade actions and uncertainty around what may be next. Heightened uncertainty about future trade policies is directly reducing business investment, and there is a risk that this will spread to households as well. These consequences can be buffered through easier monetary policy, and many central banks have recently eased in response. However, we need to remember that tariffs and trade restrictions will work over time to permanently reduce potential output everywhere, while raising the prices of consumer goods—a stagflationary scenario. Monetary policy can only do so much about these elements of the shock.”

(The Monetary Policy Report contains even more detail and quantification of the risks – it ain’t pretty! In particular, see pages 19-21)

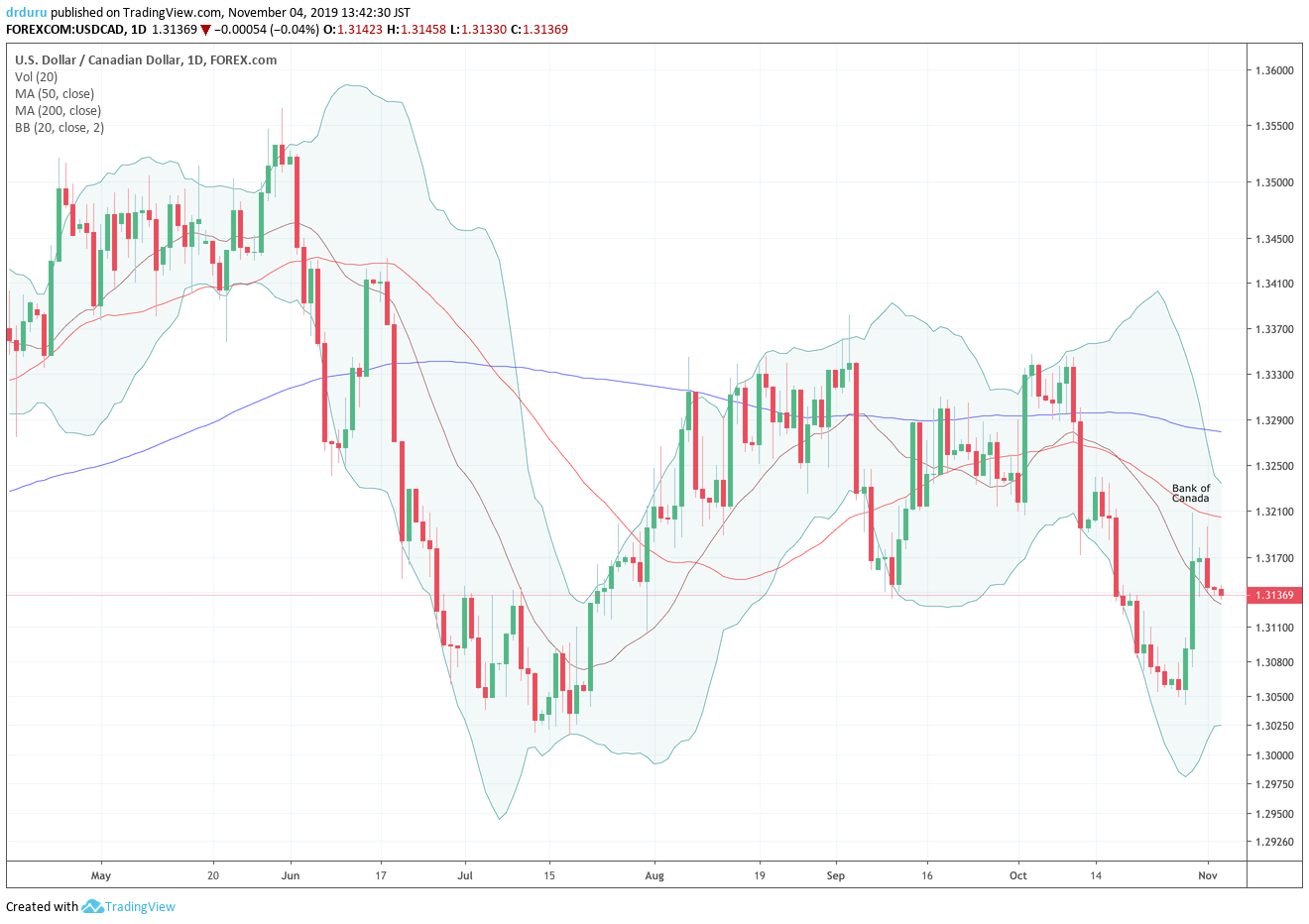

These warnings were enough to significantly weaken the Canadian dollar.

Source: TradingView.com

The sharp rebound in USD/CAD meant that I did well to take profits on my short USD/CAD position as it approached support at the July lows. Given I remain bullish on the Canadian dollar (bearish USD/CAD), I faded the rally. I plan to accumulate a larger short USD/CAD position up to the August/October peaks. Note that USD/CAD continued its slide in the wake of the Federal Reserve announcing its latest stance on monetary policy hours after the Bank of Canada announced.

I remain bullish on the Canadian dollar even as Poloz made sure to call out the risks to the Canadian dollar:

“the biggest effect for Canada of a more negative global growth scenario would be a steeper drop in commodity prices and, as in 2015, a significant depreciation of the Canadian dollar.”

I assume the more explicit references to the currency are reactions to the (unwelcome) appreciation in the Canadian dollar in recent month. Yet, until the risks materialize (or the market decides to more aggressively price in the risks), Poloz himself gives me reason to think of the Canadian dollar as more attractive than numerous alternatives (emphasis mine):

“In contrast to these adverse global developments, the Canadian economy is demonstrating resilience overall. The economy continues to create new jobs at a solid pace, the unemployment rate is near an all-time low, many companies are reporting an acute shortage of skilled workers, and wage growth is picking up noticeably in the past six months or so. The housing sector is clearly on the rebound…Consumption spending has held up relatively well on average, supported by the solid labour market and low interest rates, even as the savings rate has been edging higher…

On the whole, however, it appears that our economy is still operating close to capacity but probably with a modest amount of excess supply.

Governing Council agreed that, all things considered, this excess supply is probably not pervasive. Furthermore, our situation differs from many other countries in that inflation is at our 2 percent target today and projected to remain very close to target, despite the presence of modest excess supply.

The Bank of Canada’s walk along the precipice of pessimism begged the question that one reporter asked: “How close did you come to cutting rates?” Poloz responded essentially with a reiteration of all that is good about the current Canadian economic situation: “We definitely talked about what that would look like. So far, we can clearly identify a drag from the trade side, but we also have some pretty good lift from other parts of the economy. We start this discussion with inflation already at target. Here we’re talking about something intangible: trade frustration and uncertainty.”

Not satisfied, another reporter asked “Did Bank consider an insurance cut?”, a not so subtle reference to the Federal Reserve’s headline excuse for cutting interest rates while the U.S. economy remains on solid footing. Poloz’s response was telling. After a long bout of hesitation, he finally said “…unless a risk becomes obvious, more inclined to understand something better. There are all kinds of things changing at once. The answer is no.” I interpret that response as meaning HE may have considered proposing it, but the Governing Council as a whole did not consider it. An insurance cut could certainly come into play if the Bank of Canada gets some room from a decline in inflation. In other words, inflation numbers may become the key indicator in the coming months of what the Bank of Canada may do.

Be careful out there!

Full disclosure: short USD/CAD