“Uncertainty about the global outlook is undiminished, particularly with respect to policies in the United States.” – Bank of Canada press release, “Bank of Canada maintains overnight rate target at 1/2 per cent”, January 18, 2017

I start with this quote from the Bank of Canada because it stands in stark contrast to global financial markets, especially in the U.S., that have behaved with a good deal of certainty. This stance forms the basis of the abundance of caution expressed throughout the Bank of Canada’s decision to hold interest rates constant at its last pronouncement on monetary policy. Amid the caution, the Bank of Canada slightly increased its growth assumptions for the U.S. by 0.5% through 2018 because of an anticipated mix of corporate and personal tax cuts. Forecasts for Canada stayed “largely unchanged” because “in contrast to the United States, Canada’s economy continues to operate with material excess capacity.” The Bank of Canada boosted its Canada growth rate just 0.1% through 2018.

The Bank summarized Canada’s growth prospects as follows…

“While employment growth has remained firm, indicators still point to significant slack in the labour market. The resource sector’s adjustment to past commodity price declines appears to be largely complete, but negative wealth and income effects will persist. Meanwhile, the Canadian dollar has strengthened along with the US dollar against other currencies, exacerbating ongoing competitiveness challenges and muting the outlook for exports. Consumption is expected to remain solid, while residential investment will be tempered by previously announced changes to housing finance rules and by mortgage rates that have risen in response to higher bond yields. Federal and provincial fiscal measures are still expected to support growth in 2017.”

Bank of Canada governor Stephen S. Poloz provided more background on the process of assessment in the opening statement to the January Monetary Policy Report. I was most interested in the Bank’s views on the impact of potential changes in U.S. economic policies. Poloz confirmed that the Bank is worried about U.S. President Trump’s trade posturing, but specifics remain elusive and thus not yet calculable.

“In our discussions, Governing Council was particularly concerned about the ramifications of US trade policy, because it is so fundamental to the Canadian economy. But we cannot capture these in our projections because they are simply unknown at this point.”

In the accompanying Monetary Policy Report, the Bank of Canada further emphasized its concern about Trump’s trade posturing and the parallel difficulty in assessing it right now:

“While prospective protectionist trade measures in the United States would have material consequences for Canadian investment and exports, these measures have not been included in the base case.”

In thinking through the relatively clearer prospects for tax reduction in the U.S., the Bank outlined three likely downsides that temper the positive of increased U.S. disposable income to buy Canadian exports…

- A corporate tax cut will reduce the competitiveness of Canadian exporters.

- Bond yields have increased in anticipation of the stimulative impact of tax cuts. These yield increases have flowed back into the Canadian economy where on-going slack requires lower rates, not higher. The unwanted to increase in rates will create a drag on the Canadian economy.

- The U.S. dollar has surged along with rates. The Canadian dollar has largely kept up with the U.S. dollar (going into the monetary policy decision) which will create an additional drag on export competitiveness.

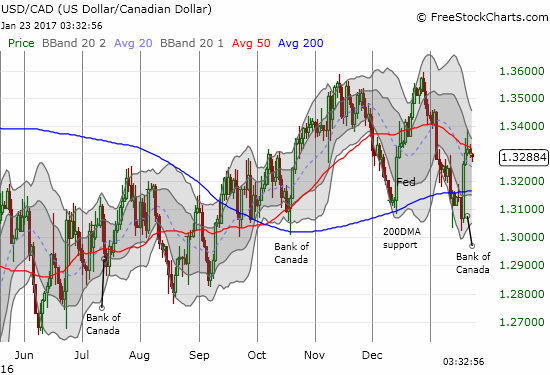

The Bank of Canada made it abundantly clear that it still wants and needs a weaker currency. With U.S. actions providing net headwinds to the Canadian economy, the Bank of Canada will certainly tip-toe around any rhetoric that might motivate buyers in the currency. It is no accident that the market responded to the Bank of Canada’s monetary policy report by selling the Canadian dollar. The selling lasted three good days.

Source: FreeStockCharts.com

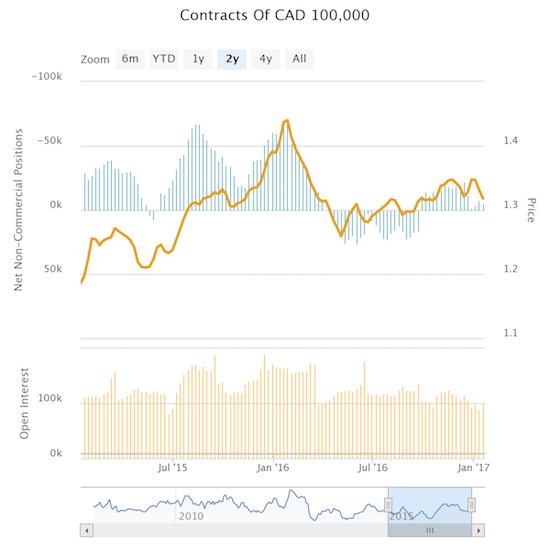

Source: Oanda’s CFTC’s Commitments of Traders

During the press conference (around the 31:00 mark), Poloz explained that, historically, when the U.S. dollar strengthens, traders assume that whatever is good news for the U.S. is also good news for Canada. This linkage takes the Canadian dollar up with the U.S. dollar. However, in the last two to three years, Canada experienced a “terms of trade shock” thanks to plunging oil prices that the U.S. experienced as a net positive. Poloz thus implied that traders have the incorrect calculus if they are holding the Canadian dollar aloft because of dollar-positive catalysts in the U.S.

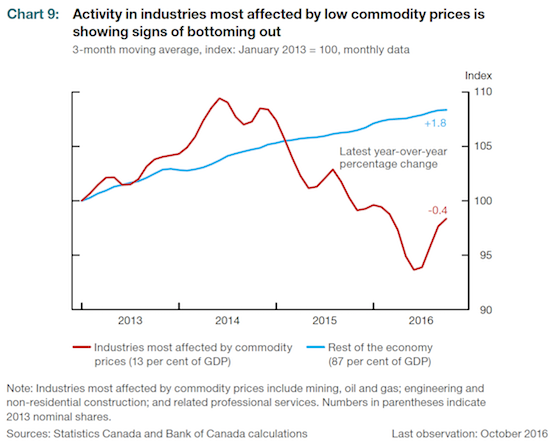

There IS good news on Canada’s economic growth. The non-commodity part of the economy has experienced a near steady growth rate since 2013. The commodity part of the economy topped out in 2014 along with oil prices. However, 2016 was a year of recovery that the Bank assumes will continue will into 2017.

Source: Bank of Canada Monetary Policy Report, January 18, 2017

Taken together, I think all the data and rhetoric point to a Canadian dollar that will continue grinding away in a loose range with a slight bias toward weakness against the U.S. dollar. The Bank of Canada seemed to awaken traders to the net bearish outlook for the Canadian dollar. Moreover, President Trump has officially declared his intent to renegotiate the North America Free Trade Agreement (NAFTA) with Mexico and Canada on terms more favorable to the U.S. Such actions should be a net positive for the U.S. dollar and net negative for the Canadian dollar. In turn, a poorer trade position will force an export-sensitive Bank of Canada to speak even more dovishly in future monetary policy decisions.

Full disclosure: long USD/CAD