The Bank of Canada released its latest pronouncement on monetary policy on the heels of a rapid rally for the Canadian dollar (FXC). USD/CAD was down 5 straight days going into the release of the January, 2019 Monetary Policy Report. Four of five of those days delivered substantial declines.

Source: TradingView

The Bank provided a truncated summary of the Monetary Policy Report in the following one-minute silent video.

The Bank of Canada left its interest rates as-is given a thick soup of economic headwinds and tailwinds. Lower oil prices dropped the forecast of GDP growth for 2019 from 2.1% to 1.7%. Trade tensions between the U.S. and China and increased tariffs also threaten to lower projections for global growth and trade. Lower than expected consumption spending and housing investment along with subpar wage growth are also weighing on the economic outlook. However, Canada should benefit from a strong group of counteracting tailwinds:

These developments are occurring in the context of a Canadian economy that has been performing well overall. Growth has been running close to potential, employment growth has been strong and unemployment is at a 40-year low. Looking ahead, exports and non-energy investment are projected to grow solidly, supported by foreign demand, the CUSMA, the lower Canadian dollar, and federal tax measures targeted at investment.

Governor Stephen Poloz summed up the situation in his extensive opening statement as follows:

A lot has happened since our last MPR in October. For one thing, the US-led trade war is beginning to have negative economic consequences. Global financial markets have reacted—bond yields have fallen, yield curves have flattened even more and stock markets have repriced significantly. Here in Canada, lower oil prices have reached the point where they will have material consequences for our macroeconomic outlook. And, our housing sector is taking longer than expected to stabilize…

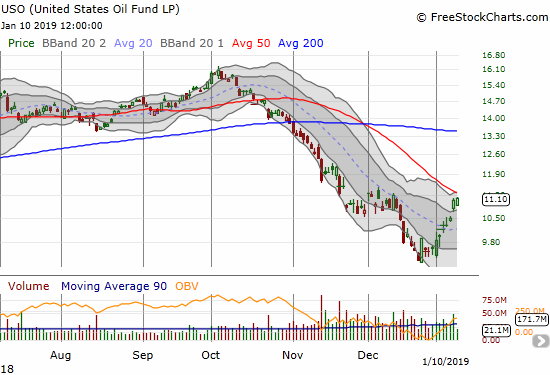

The bulk of Poloz’s statement was spent describing all the headwinds facing the Canadian economy. As a result, the statement sounded very dovish. The subsequent press conference stayed on message. Perhaps Poloz intended to sound dovish given the recent surge in the value of the Canadian dollar. Much of this surge has no doubt occurred because of the rapid rise in oil prices. This surge is helping the Canadian dollar to continue pushing USD/CAD lower and right past the Bank’s dovishness.

Source: FreeStockCharts.com

Given the Bank of Canada’s effective dovishness, I do not expect USD/CAD to sustain a breakdown below support at its 200-day moving average (DMA). I also suspect oil will take a “rest” soon. As I stated in an earlier post, I flipped to bearish on the U.S. dollar (DXY). Part of that bearishness sat in a healthy-sized short position against USD/CAD. I did not risk the profits to the Bank of Canada, and I am now on the sidelines. I am willing to fade USD/CAD on its way to a rendezvous with the 200DMA, and I will reassess at that time.

Be careful out there!

Full disclosure: net short the U.S. dollar index