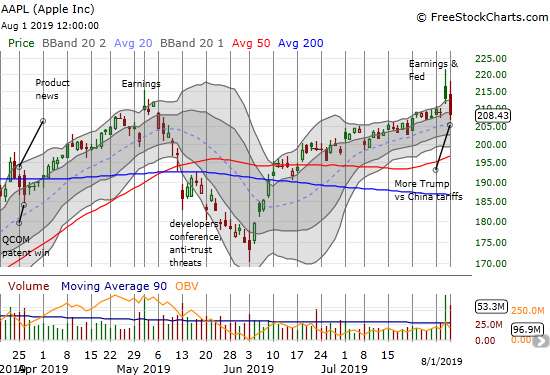

The bullish post-earnings scenario I painted for Apple (AAPL) worked out relatively well in the first day of trading. After AAPL quickly topped out, my proposed strategy for a calendar call spread rapidly transformed from under-performing the benchmark weekly $210 call strategy to outperforming.

In the immediate wake of earnings, AAPL gapped over expected $215 resistance for a 6.0% gain. APPL closed the day with just a 2.0% gain. AAPL went from far surpassing my expectations to nailing them. AAPL was off to the races again the next day until President Trump announced a 10% tariff on $300B more of Chinese imports. Apple (AAPL) promptly lost 2.2% for the day and closed right where it was before reporting earnings July 30.

Pre-Earnings Setup

After AAPL traded down as much as 1% ahead of earnings, I received my trigger to refresh my bullish pre-earnings positioning. After buying call spreads, I decided to add a weekly calendar call spread using the $215 strike because it was so “cheap.” I paid just $0.35 for the spread which meant I had little downside risk and a lot of upside potential.

The Intraday High

Because AAPL was tossed around about by different catalysts, I break the post-earnings assessment into three parts: 1) The path to the intraday high immediately after the post-earnings open, 2) the immediate post-Fed reaction and the counter-reaction, 3) the post tariff reaction.

Source for charts: FreeStockCharts

AAPL gapped over the $215 resistance line that I thought would cap post-earnings gains. While this was great for the call spread I bought to make a bullish bet on AAPL, it was not ideal for the calendar call spread. Once AAPL hit $220, I decided to take the profits on the calendar call spread. The value had nearly doubled, but I feared if I sat on the spread much longer, the profits would start to erode as AAPL went higher.

Ironically, the calendar call spread held steady as AAPL drifted lower. The benchmark $210 weekly call drifted lower along with the stock. By the end of the day, the benchmark lost all its gains.

Source for data: Etrade Options

The Powell Plunge

The Federal Reserve delivered some mixed and confusing messaging in delivering its statement on monetary policy. After Chairman Jerome Powell made clear the Fed was not launching a rate cutting cycle, the stock market threw a temper tantrum. The “Powell Plunge” sent the volatility index (VIX) soaring higher, and ALL options got a boost. For example, my calendar call spread increased in value: the impact of increased volatility was greater on the long side (expiring next week) of the spread than the short side (expiring this week). While AAPL closed well off its high in a “gap and crap” pattern, my call spread did not change much in value throughout the day and the calendar call spread closed near a high for the day.

Apple’s earnings took the market and analysts by surprise. Assuming that a lot of analysts will need to upgrade AAPL, I started a fresh post-earnings trade after the dip. I bought a weekly calendar call spread at the $220 strike, and near the close I added another long $220 weekly call expiring next week. I basically used this week’s $220 call options to help pay for my next weekly call trade on AAPL.

Fresh Trade War Drama

All looked well when AAPL sprinted out the gate at the open on post-earnings day number two. The stock market was positively re-evaluating its disappointment over the Fed’s performance, and buyers were rushing in to scoop up the “bargains” created by the Powell Plunge. President Trump sideswiped the market around 1:30pm Eastern when he announced a 10% tariff on the remaining $300B of Chinese goods exported to the U.S. AAPL immediately sold off even though CEO Tim Cook the previous day reassured the market about business in China. From the Seeking Alpha transcript:

“I’d like to provide some color on our performance in Greater China, where we saw significant improvement compared to the first half of fiscal 2019 and return to growth in constant currency. We experienced noticeably better year-over-year comparisons for our iPhone business there than we saw in the last two quarters and we had sequential improvement in the performance of every category. The combined effects of government stimulus, consumer response to trade-in programs, financing offers, and other sales initiatives and growing engagement with the broader Apple ecosystem had a positive effect. We were especially pleased with a double-digit increase in services driven by strong growth from the App Store in China…”

After the dust settled, AAPL finished a swing from just under $218 to just under $207. The stock ended the day with a 2.2% loss. With a close at $208.43 and the VIX soaring to 17.9 (it went as high as 19.5), the $215 calendar call spread I sold had only lost about a tenth of its value from the previous day’s close. It was STILL worth more than my original selling price!

The benchmark $210 call spread lost 75% of its value and is likely headed for a worthless expiration. Of course anyone following the benchmark strategy should have sold into the initial gap up on the post-earnings open. My calendar call spread is essentially back to its original value, and I have two more weeks to wait out a potential rebound.

Lessons learned

While other catalysts impinged on the AAPL pre-earnings trade, I am overall satisfied with my interpretation of the implications of AAPL’s earnings trade history. The combination of extreme analyst bearishness alongside bullish historical correlations turned the AAPL pre-earnings trade into a very good risk/reward proposition. This experience demonstrated once again the potential of trading against the grain when that grain gets extreme. I also received a powerful reminder of the attractiveness of calendar call spreads when volatility is on the rise.

Be careful out there!

Full disclosure: long AAPL put spread, long AAPL calendar call spread, long AAPL calls, long UVXY calls