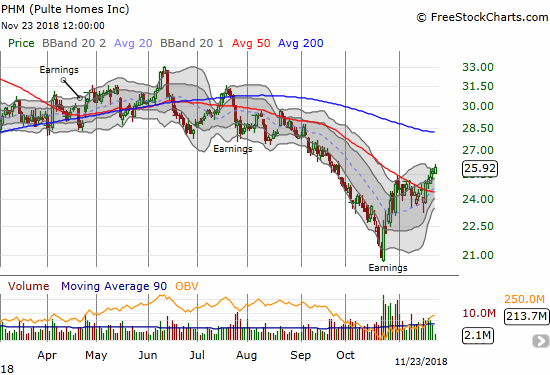

Pulte Homes (PHM) reported Q3 2018 earnings on October 23rd. The stock responded favorably with a 7.3% one-day gain. That same day, the S&P 500 (SPY) gapped down and sold off for four more trading days. The index now sits at a near 7-month low while PHM is holding an impressive 24.1% total post-earnings gain. This relative out-performance is consistent with the seasonal strength of home builders (running from November to March), but the behavior is quite contrary to the habitual post-earnings selling the plagued home builders for much of the year. Even after the market returned to post-earnings punishment in response to earnings from KB Home (KBH), PHM recovered all its sympathy losses and then some the very next trading day. Together, these performances make PHM one of my prime targets for buying into the seasonal trade on home builders. I now own shares, and I am looking to accumulate call options.

Source: FreeStockCharts.com

The headline numbers in the earnings report showed strong financial performance:

“For the quarter, the Company reported net income of $290 million, or $1.01 per share compared with prior year net income of $178 million, or $0.58 per share. The higher net income for the period was primarily the result of a 25% increase in homebuilding revenues, in combination with a 190 basis point expansion of operating margin.”

PHM tried to address growing concerns about the housing market head on and assuage those fears:

“While buyer concerns around affordability and rising mortgage rates appear to have impacted near term market dynamics, traffic trends indicate that buyer interest levels are still high and that the overall housing recovery remains on track.”

We now know the commentary on traffic trends directly contradicts the sentiment of builders in general in November, so this part of PHM’s confidence is on watch for confirmation in the next earnings report. In fact, these claims form a large part of the investing thesis in PHM in spite of deteriorating housing data.

PHM also expressed confidence in the value of the company by purchasing 2.4M shares for $67M during the third quarter. The average price of $28.14/share of course turned out to be a significant premium with the stock still trading comfortably below that level.

I found additional useful insights from reading the transcript of the earnings call.

The concerns over the health of the housing market are clearly palpable for PHM management as the CEO tried to address these worries at the very start of the conference call. He even referenced the weakness in the stocks of home builders as evidence of the concerns:

“I would typically focus my opening comments on the strength of our Q3 numbers. But when housing stocks drop over 20% during that same period, it may be more useful to start with the review of market conditions as this seems to be an area of focus for our investors. Based on industry dynamics, we maintain our positive view on the housing market and the overall sustainability of the current housing recovery. We fully appreciate, however, that operating conditions have changed over the past several months…

In what we view as a good operating environment, but one that is arguably more challenging than 6 to 9 months ago, we are well positioned to deliver ongoing financial success.”

Those were the bookends of the summary. The summary was laced with some very real blemishes. Moreover, the summary leaned heavily on the same macroeconomic trends and strengths that are well-known and have yet to reverse the slowdown in the housing market. Here are my key bullet points from the CEO’s summary (in between the bookends):

- Buyer interest high: Q3 buyer traffic +15% year-over-year, accelerating through the quarter.

- Affordability becoming a bigger issue: absorption pace/conversion rate down, feedback from sales teams. Talked about lower conversion rate in last earnings call when mortgage rates started increasing in May.

- Market conditions more competitive.

- Macro-economic data are strong and housing supply remains tight.

- Period of adjustment will smooth over current challenges: “…some combination of adjustments in price and/or income or simply even just the passage of time should help consumers to get over these hurdles.”

During the Q&A, management pointed to year-over-year gains in website traffic as a leading indicator of strong customer demand. Management also saw encouraging signs for the start of Q4: “Demand conditions through the first few weeks of October are consistent with trends that we saw in Q3 as high levels of traffic demonstrate ongoing buyer interest, but with consumers taking longer to make their purchase decision.”

The quality of customers also remains high; they are not over-stretching to buy a home.

“Our can [cancellation] rate was just under 15%. That’s actually slightly lower than where we were prior year. ARM usage sits at 5%, which is down from where we were in the prior quarter. So we haven’t seen a huge increase in ARMs. I think that has to do with the yield curve. There’s not enough differential on the long part of the yield curve. Loan to values are still well within kind of the range that we’ve been operating in for the last couple of years. And credit scores for us, the loans that we actually financed through our mortgage company remain high.”

Having said all this, PHM still had to soften its margin guidance for the fourth quarter. This action sets up a lot of suspense for full-year 2019 guidance in the Q4 earnings call (emphasis mine).

“Given the composition of our production pipeline, we expect fourth quarter deliveries to be in the range of 6,500 to 6,800 homes, which would put us within our guidance for full year closings of 22,500 to 23,500 homes. Based on our backlog and current production schedule, we expect our Q4 average sales price to be in the range of $420,000 to $430,000. This is a slight adjustment from our prior guidance of $415,000 to $425,000.

Given that overall market conditions have gotten more competitive, we expect Q4 gross margin will likely come in towards the lower end of our previous guidance range of 23.8% to 24.3%.”

I am surprised this reduction alone was not enough to clobber PHM’s stock. Margin slippage has often undermined home builders (like KBH). During the Q&A, management provided additional color on its approach to margins in this new competitive environment:

“We’re not going to overreact by giving away all of the margin that we’ve worked so hard to earn, but we’re going to make the decisions that we need to make to make sure that we’re continuing to turn the inventory…I think you saw our gross margins in Q3 come in near the lower end of our guide, and that’s reflective of the fact that we did put some additional incentives in place to help move order growth…

So one of the reasons we moved our guide down on margin in Q4 was that’s when we’ll feel the real brunt of that push-up in pricing early in the year.”

So far, PHM is talking about relatively minor margin pressure. The company is staying optimistic because it thinks it has options before resorting to more significant margin hits. First of all, customers have options for getting their pricing down:

“We do feel like we’ve got good offerings in the product portfolio that we have that allows consumers to make changes either in the structural options that they add to the home or maybe don’t add to the home. They also have the ability to move up and down within the square footage range that we build within that community. So I think we’re pretty well-positioned there.”

The company has prioritized its own options by putting margin hits at the bottom of the list of actions it might take to respond to market pressures:

“As far as things that we can do, there are clearly incentives that we can offer as it relates to option packages, lot premiums. There’s financing incentives that we can offer to help alleviate some of the pressure that we’re feeling around overall affordability. And then, of course, the easiest thing potentially to do and sometimes the most painful from a profitability standpoint is just absolute base price adjustments, and we tend to go there last, is kind of the order of magnitude of change that we would typically make…

With traffic in our stores, we believe it’s a matter of effectively responding to buyer concerns, real and perceived, to generate stronger sales in future periods.”

The brightest spot in PHM earnings, by far, is the robustness of demand for the “active adult buyer” market segment. This segment consists of older adults who do not want/need to live in assisted-living communities but do want to live among neighbors in their similar age group and activity level. These customers clearly have a lot of money to spend, and their demand for housing is growing. I assume these dynamics are a result of baby boomers selling homes in expensive markets and buying comfortable “retirement pads” with cash to spare to support their active lifestyles.

“All of the conversation has kind of moved to the millennials and to the entry levels, but there is still a lot of boomers out there, they have high homeownership rates. And this is a buyer group that, for us anyway, 40% of them pay cash, and so they’re much less interest-rate sensitive, which works to our advantage…

Signup trends by buyer group in the third quarter were similar to what we experienced in Q2 of this year, as first-time orders declined 13% from last year to 1,373 homes, while move-up orders were down 1% to 2,456 homes. Demand among active adult buyers remained exceptionally strong in the third quarter as orders increased 22% over 2017 to 1,521 homes…

By buyer group, absorption pace among first-time buyers was down 21%, which reflects the impact of slower sales pace, as I referenced in our Southeast and Northern California markets. While pace decreased 7% among move-up buyers and increased 9% among active adult buyers.”

Obviously PHM cannot thrive solely on the robust demand of its active adult buyers, but it is a source of business that gives PHM an advantage over other home builders.

In the end, PHM is putting on the typical brave face as the company stares down deteriorating conditions in the housing. This quote summarizes the attitude:

“We still think that the underlying fundamentals of the market are strong, we’re certainly in a little bit of a tougher period of time right now. But I don’t know that I would expect that to continue for an extended period of time.”

This brave face looks good paired with an out-performing stock. My bet on PHM presumes this out-performance equates to a lower risk profile. The valuation is not rock bottom, but I missed those levels directly ahead of Q3 earnings. PHM’s price/book ratio is still at 1.6; rock-bottom valuation would be 1.0 and lower. PHM’s earnings and sales ratios are essentially rock bottom though: trailing P/E is 8.8, forward P/E is 6.9, and price/sales is 0.7. From here until the most recent low, I will buy the dips with call options. I set my upside price target on PHM around the summer highs from $30 to $31/share. I do not expect PHM, or any other builders, to make more progress than that without notable improvements in the housing data and the stock market in general.

Be careful out there!

Full disclosure: long PHM