For the past few months, I pestered my youngest brother to write a review of his cogent 2009 analysis of the housing market. In that post, he predicted housing would bottom in April, 2010 and as late as 2013 in a worst case scenario. He has finally produced the follow-up, and I post it below.

In his latest post he posits the housing bottom was actually in March, 2009 but prices will bounce along the bottom until 2013. He was also kind enough to examine each of his prior predictions for their accuracy. Of course, it is always more fun to conduct such an exercise when you nail most of the analysis. I expected nothing less from him.

The following analysis contains his own words with some editing from me. I am just as convinced as I was last year, and I am thrilled he is too busy to bother blogging so I get to post his work here. (Note well that this was written before Tuesday’s release of the latest Case/Shiller Index).

=====================

Re-Re-Examining the April 2010 Home Price Bottom Prediction

When housing prices started to decline dramatically around 2008, I made a prediction of a national home price bottom in April of 2010 based primarily on looking at patterns of home price declines in regional recessions over the last 30 years.

In August of 2009, the home price decline appeared to be more severe than most predictions (including mine). The May 2009 Case-Schiller Housing Price index data was the most recent available at that time. It showed an 18% y-o-y decline in national prices, and it showed a 0.5% m-o-m increase – following 22 months of consecutive monthly declines. There was an emerging debate about whether or not shadow inventory existed, and whether the banks were intentionally delaying foreclosures to keep that shadow inventory at bay. Mortgage delinquencies were at a post-Depression high of 6% and increasing in parabolic fashion. Loan modification programs were operating, but their success was in doubt. Unemployment was above 9% and still rising. The one bright spot was that the stock market was 50% off of its March 2009 lows.

In this environment of uncertainty in the fall of 2009, I re-examined my April 2010 housing price bottom thesis. I looked at home prices taking into account employment, mortgage delinquencies, walk-aways, civil unrest, interest rates, and behavioral economics. After this analysis, I stuck with my April 2010 bottom thesis with the additional caveat that home prices would probably stay nominally flat through 2013.

This post re-examines these predictions.

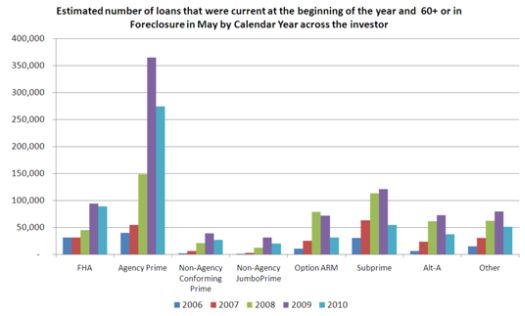

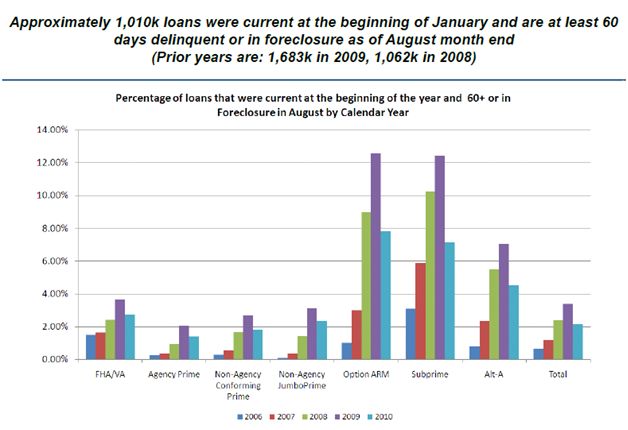

There is still a lot of bad news in the housing market. However, the drops of good news in the housing market are instructive about its future direction. First, let’s look at the number of loans that were current at the beginning of the year and are 60+ days delinquent or in foreclosure in May. This is shown below from 2006 to 2010 – first for May 2010, then for August 2010. This is provided courtesy of LPS Mortgage Monitor June 2010 Mortgage Performance Observations. The good news is that across all loan types, the number of new delinquencies is down. Using a trend line for either of these two months, it seems reasonable to assume that by 2012, new delinquencies will return to normal.

(Click for a larger view)

Source: LPS Mortgage Monitor June 2010 Mortgage Performance Observations

LPS also provides data on the number of loans that are delinquent, in foreclosures and REOs – the so-called shadow inventory. As of August 2010, this shadow inventory was about 7.3 million. This is 10% less than the January 2010 peak of 8.0 million and roughly equivalent to the 7.2 million of August 2009. So this is trending in the right direction.

We can now much more clearly estimate the time to clear the shadow inventory. The 7.3 million in shadow inventory now will be joined by another 700,000 in new delinquencies through the end of 2011. This brings the total delinquencies to 8.0 million. Perhaps 1 million of those loans will “cure” through borrowers getting current and successful loan modifications. This leaves 7.0 million homes in shadow inventory. A normal level of shadow inventory seems to be somewhere around 1 million. So we’ve got an excess of 6.0 million in shadow inventory.

Source: LPS

RealtyTrac reports that 33% of all homes sold are REOs, short sales, or delinquent. Factor this in to the roughly 5 million in total home sales where we seem to be trending, and these sales equate to a 1.7 million annual decrease in the shadow inventory per year. That means it will take 3.5 years to burn off the excess shadow inventory based on these trends. This is consistent with the flat home prices I projected through 2013. I still think this is the most likely scenario. The best case scenario includes home sales of 6 million in 2011 and 2012 combined with 50% of these sales as shadow inventory. Even under this optimistic scenario, it will take 2 years to burn off the inventory. Based on this analysis, I am sticking with my thesis of flat home prices through 2013.

Now for two caveats…

Caveat #1: The March, 2009 Bottom

The one thing I know for sure is that my prediction of an April 2010 bottom is wrong. At least, it is wrong according to my favorite home price tracker, the Case-Schiller Housing Price Index. According to this index, a bottom was achieved in March 2009, and we are actually already up 7% above these lows. It seems unlikely that we will decline enough to crack this low. Fall and winter are the traditional home price decline seasons, but in the Fall of 2009 and the Winter of 2010, the declines were only 2%. Prices could decline 10% from here and technically establish a new low in March/April, 2011. However after the 32% decline from the housing price top to the March 2009 bottom, this kind of price adjustment is mainly noise. For all practical purposes, the bottom was achieved in March 2009 and it is looking like a sideways trend through 2013.

There is no double-dip in housing on the horizon. Unless unemployment gets worse, housing will continue to stabilize. There is no cause to worry unless weekly claims go above 500,000 or if the total number of people employed shrinks. The shadow inventory is large at 7+ million, but it is ironically not distressed inventory. The big banks are the ultimate owners of this inventory, and they can hold these for several years without any financial strain. I reviewed the earnings report presentations of the big banks, and none of them are pressed to dump this inventory or raise cash. Most of them actually had significant reductions in their reserves for loan losses indicating that they are not concerned about the potential losses from this inventory. Unless banks start to scramble for cash, this inventory will continue to be released slowly without significant damage to home prices.

Caveat #2: National vs. Local Prices

This analysis only refers to national prices, and cannot be extended to local home prices. Home prices are diverging radically between cities. Prices can even diverge dramatically within a single city. For example, Case-Schiller shows home prices up in the S.F. Bay Area by 21% year-over-year. On the other hand, prices in New York hit a new low in April 2010, and six other metro areas had new lows in March 2010. In Atlanta – the only market I track at the sub-market level – some zip codes have half as much inventory as they did 2 years ago, and others have 20% more than last year. You can imagine how these inventory balances impact prices in these two zip codes. If you are thinking of buying or selling a house right now, you have to know your city and your neighborhoods to know whether the time is right.

Lastly, A Detailed Retrospective

For therapeutic reasons, I also re-examined my September 2009 conclusions one-by-one with new commentary shown below in bold. This retrospective doubles the writing, but it is a worthwhile exercise given few people return to previous predictions to review their accuracy (or lack thereof). Some of the points below are similar to those listed above.

- Sept, 2009: “We have not bottomed yet in terms of prices. They will fall through the fall and winter. There are too many headwinds in terms of unemployment, delinquencies, oversupply, and buyer sentiment.”

Right and Wrong. I was actually right that prices would decline through the fall of 2009 and winter of 2010. However, the increase during the spring/summer of 2009 was greater than that decline. Therefore, the Case-Schiller index bottom in March 2009 has held and my prediction of a bottom in April 2010 has proven incorrect.

- Sept, 2009: “I am going to stick with my housing price bottom in April 2010. However, I recognize a worst case scenario based on delinquencies turning into foreclosures that overwhelm the housing market that would push the housing price bottom out to April 2013. But even in this worst case scenario, prices will not fall anymore than 10% beyond wherever prices are in 2010, because most of the damage will have been done.

In the best case scenario, the bottom in 2010 will be followed by three years of slow price growth (say around 2%) until at least 2013. More likely, nominal prices will bottom in 2010 and nominal prices will remain relatively flat through 2013 and then start to increase again. I realize that this still equates to a decline in real terms, but at least over this three year period, most homeowners will be building equity and also most homeowners think in nominal not real terms when it comes to the price of their house.”

I was right not to push my bottom further in the future than April 2010 (as many others have done). I also am sticking with my flat prices through 2013 prediction.

- Sept, 2009: “The Fed will be under enormous pressure to keep interest rates as low as possible through at least 2013 because of housing alone. This will be true even if prices start to rise in the rest of the economy. It is hard to imagine any situation other than serious inflation by 2013.”

Right (so far). A recent regional Fed study indicated that the Fed should keep interest rates near zero through the end of 2011. I am expecting it will take at least one more year than that to ensure the housing market stabilizes.

- Sept, 2009: “We ain’t seen nothing yet in terms of foreclosures. This is just getting started. My best case scenario has 4 million foreclosures in 2010, 2011, and 2012. The historical data are not good on this, but we could get more foreclosures than we had in the preceding 20 years combined. I am declaring 2010 to be the “Year of the Foreclosure” as loan modifications will certainly be slow to clean up the delinquencies that are already in the pipeline. But with midterm elections in the same year, expect a lot of public anger, political rhetoric, and a bunch of legislative actions to try to stop foreclosures. Obviously, it is unclear how this will impact things, but I am guessing not much based on recent history.”

Right about foreclosures increasing. The actual foreclosure level looks like it will to be much closer to my worst case scenario of 7.5 million rather than my best case scenario of 4 million. 2010 was the year of the foreclosure. I am declaring 2011 to be the year of the REO.Wrong about anger, rhetoric and legislative action. I suspect that as people have gotten to the other side of a foreclosure, they are probably much better off, and therefore do not have much to complain about (relatively speaking of course).

- Sept, 2009: “I have no insight on whether or not banks are intentionally slowing the progression of homes from delinquency to REO. The banks would not admit to it, even if they were. The gap between delinquencies and REOs is notably large, but it is unclear why. More importantly, I do not think I have a problem with banks holding back REOs. I would definitely rather have them focus their resources on loan modifications rather than dumping more houses on the market.

Ideally, they will keep inventories high enough to scare off the builders from adding new supply (10 months of supply, which is where we are now, is enough to do that), but not so high that home prices fall through the floor again (anything over 12 months will lead to more serious declines). If you believe that banks are intentionally holding back supply, then you would also believe that prices will stay flat between 2010 and 2013. This is as quickly as all the foreclosures can be processed without further damaging housing prices beyond where they will end up in Spring 2010. This actually tends to favor the Spring 2010 bottom scenario and the flat through 2013 scenario.”

I think the most important thing to understand about the housing market right now is that the big banks (Wells Fargo, B of A, Citibank, Chase) very much control it. This is done by controlling the speed at which they process foreclosures and the levels where they price REOs. This stands in stark contrast to the standard housing market which was highly fragmented on the supply side with no individual holding much inventory.

- Sept, 2009: “There will be no need to build any significant number of new houses until at least 2014…sorry Toll Brothers (TOL). New home sales (not prices) may have bottomed, but they definitely will not increase anytime soon. The “newish” inventory from homes built from 2005 to 2007 are coming back on the market and will be a suitable replacement for the new home market.”

Right. Home sales have more risk to the downside than any opportunity to the upside. There really is no such thing as a new home market. There is just a housing market. In the pre-housing crash days, demand for houses outstripped supply. This created excess demand that was soaked up by builders creating new houses. Today, the housing market supply is much higher than demand and likely to stay that way for years. Therefore, there is no need to build new houses. I am sticking with 2014 as the next year that there will be an uptick in new home sales.

- Sept, 2009: “The numbers to watch are mortgage delinquencies (tracked well) and loan modification success rates (not tracked well). If 60-day mortgage delinquencies look like they are going to crack 12%, get worried and take another look at the situation. And we need to keep hunting for reliable and credible loan modification data.”

Right things to track. Loan modifications have been negligible in the face of the 7 million homes delinquent or REOs. Delinquencies never hit 12%, so no need to significantly revise down the housing price bottom.

- Employment Perspective

Sept, 2009: “Several months ago, I looked at monthly employment rates and home prices in San Diego in the early 1990s recession to see where they bottomed. Home prices bottomed 18 months after unemployment reached a high. At first I was surprised by this lag, but it makes sense since a lot of people are rehired at lower paying jobs and ultimately still have to sell their houses quickly. If you assume that in the current cycle, unemployment peaks in mid-2010, then the best we can hope for is an April 2011 bottom, but more likely an April 2012 bottom. The biggest problem with extrapolating San Diego in the 1990s to the current national situation is that in the current national cycle, home prices and sales started crashing well before the economy, so a lot of the marginal folks have already exited the homeowner system.”

Right. This was an interesting perspective, but as I expected slightly too pessimistic, since housing was already falling well before the recession started.

- Mortgage Delinquency Perspective

Sept, 2009: “The current 6% mortgage delinquency rate (based on 60 days delinquent) is unreal and even scarier is that the mortgage delinquencies graphs are still shooting upwards with no sign of flattening. Let us assume a worst case scenario where 15% of current mortgages default and end up in foreclosure. With 50 million homes with mortgages, that amounts to 7.5 million foreclosures. Spread the resale of these foreclosures out over three years and you get 2.5 million REOs (real estate owned) per year that will need to get sold.

Compare this with the 5 million in annual home sales where we seem to be stabilizing, and we will have REOs at 50% of total sales for 2010, 2011, and 2012. At 50% of the total market, REOs would continue to push home prices lower for three years as buyers will correctly perceive having the upper hand and will submit lowball offers to banks. This dynamic implies an April 2013 bottom. The mitigating factors here are that mortgage delinquencies may top out closer to 10% and loan modifications may get up to 25% success rates. If these two things happened, then you would have closer to 4 million foreclosures over the next three years which would not be enough to overwhelm the 15 million home sales over that period. This would make a April 2010 bottom possible, but deliver flat nominal prices through 2013, at which point they may start rising (except considering interest rates – see below). Note: I am using 3 years because foreclosures will keep chugging for a couple of years after unemployment peaks in mid-2010.”

Right. It appears my worst case scenario for foreclosures is playing out, along with my 3 years of home price pressure.

- Underwater Perspective

Sept, 2009: “I think that this is the weakest argument for why housing will be bad. Looking back at the 1990s recession again, a study found that in Boston only 7% of underwater homeowners ended up foreclosing. I expect similar results in the current national recession. At the worst, 50% of people will be underwater. If 7% of those people walk away, we are talking about 3.5% of the 50 million homes or about 1.5 million walk-aways over the next couple of years.

Note that annual existing home sales are running at about 5 million. The voluntary walk-aways make for great anecdotal stories, but they are not going to heavily impact the market the way some people fear. There are a host of reasons why a homeowner either cannot or would not walk away unless they absolutely had to. Concerns over walk-aways are more of a distraction than predictive.”

Right. People love to talk about walk-aways, but they are a tiny part of the foreclosure problem. Most of the academic measures used to estimate walk-aways are flawed.

- Civilian revolt

Sept, 2009: “As wacky as it sounds now, if mortgage delinquencies get to 15% and banks are still slow to modify loans, then we could get to a point where there is a “Tea Party” style revolt against paying mortgages, and we get massive defaults even from people that can pay. The irony is starting to sink in people’s minds that America has a financial system that is being bailed out by the general public, but then these same beneficiaries of taxpayer dollars refuse to help the public when they cannot pay their mortgages. This Tea Party could easily overwhelm the capacity for banks, courts, and governments to respond. Obviously, all bets are off at that point and anything can happen. (Note: I first wrote this a few weeks ago. A Tea Party revolt doesn’t seem as wacky anymore, but as of now anger has been directed at Obama and not the banks).”

Untested: Mortgage delinquencies never hit 15%, so civilian unrest never occurred.

- Interest rates perspective

Sept, 2009: “The scary thing about considering a bottom as far out as 2013 is that the Fed rate is unlikely to remain 0% that long. If the Fed is forced to raise its rate even to 2% at some point before 2013, it could devastate the housing market. I think the Fed would rather face inflation than deal with another downturn in housing caused by higher interest rates. This argues for a 2010 bottom, since the Fed is likely to be accommodative for a long time.”

Right. The Fed is already talking about trying to push interest rates down further in order to generate more inflation.

- Behavioral economics perspective #1 (Investors)

Sept, 2009: “I recently had a colleague ask me if now is a good time to buy real estate for an investment. Most investors and would-be investors still perceive the current situation as a buying opportunity rather than a flushing out of the market. There are still lots of people (and builders, banks, landlords, related companies, etc) holding on for dear life and until these people let go, it is hard to imagine a bottom occurring. We still have not had the real estate industry mocked the way a pets.com was in the post-dotcom bubble days.

Sentiment does not feel like a bottom yet from investors. It seems that one more leg down in prices is needed for this to happen. This may occur during the upcoming fall/winter cycle. With two more legs down, the sentiment will be sure to turn downward. This argues for a 2010 or 2011 bottom.”

Right. Sentiment feels a lot more like a bottom now. The belief in some sort of new norm rather than a V-shaped recovery is taking hold.

- Behavioral economics perspective #2 (Owner-Occupied)

Sept, 2009: “This is part speculation and part stereotype, but here it goes…Most houses are bought by couples with one spouse saying “we need a (bigger) house,” and the other spouse saying “let’s wait a year until we can save more money and get more financially stable.” In the bubble years, the financially conservative spouse would look more and more stupid every month as prices rose much faster than the couple’s income and savings. Eventually, the financially conservative spouse would give in to the other spouse and the couple would go ahead and buy, thereby reinforcing the bubble.For a couple having the same conversation now, the financially conservative spouse looks smarter every month with prices continuing to decline, especially since at least one of the spouses has likely either been laid off or has had a salary reduction or is worried that either blow is coming soon. Sometime around when employment bottoms out (in terms of size of workforce not percentage rates), the financially conservative spouse will start to lose this battle again and the other spouse will say “Ok. We’ve been saving for three years, it’s time to buy now.” This actually favors a 2010 bottom, since employment (in terms of size of workforce) will bottom some time late this year or early next year.”

On-going: The financially conservative spouse still looks like the smarter one. Even in areas such as the S.F. Bay Area where average prices are up, there are still several good neighborhoods selling at all-time lows. The earliest that the conservative spouse could be wrong is 2012. There is the possibility that the best of the REO inventory is sold in 2011.

Be careful out there!

Full disclosure: long puts on XHB and TOL (my brother holds no related positions)