Jumia Technologies (JMIA) reached another major milestone on its way to becoming a sustained factor in African e-commerce. CEO Francis Dufay announced in the Q3 earnings call that “Jumia has reached an inflection point…We are building a solid foundation for sustainable, profitable growth and the results are becoming increasingly visible”. Last week, November 13, 2025, the company sponsored an Investor Day that provided a thorough, comprehensive, and detailed review of the business. The big reveal of the day was a bold step into the future with guidance and a roadmap showing the direction of the business for the next 5 years. This bold vision shows Jumia leaping from transitioning to cash flow positive for the first time to $2.5B to $3B in GMV (gross merchandise value) by 2030 through sustained growth, representing a CAGR (compound annual growth rate) of about 25% from current levels.

With this backdrop, I was more eager than ever for my quarterly interview with CEO Francis Dufay. While I had just enough time to get through my most critical questions, the interview once again confirmed that Jumia remains on a path to reward the patience of investors who have bet on Dufay’s turnaround efforts.

This update on Jumia integrates my interview with highlights of the 3-hour long Investor Day, the Q3 2025 results, and the Q3 earnings conference call.

The Key Take-Aways for Q3 2025

Dufay ended our discussion making sure investors understand the key take-aways from Q3 results. He proudly noted that the company demonstrated the ability “to deliver significant growth, 25% in dollars on a like-for-like basis and 32% on orders, without compromising the economics, which has never happened in the company’s 15-year history.” He continued, “this performance validates the path to break-even and the business model’s value creation for customers, vendors, partners, and shareholders”. Dufay reassuringly projected that Q4 will be the first “clean quarter” in three years, “allowing for a clearer comparison of Q4 2024 to Q4 2025 improvements”. This confidence is reflected in guidance covering the next 5 years.

Guidance

A year ago, I called 2025 Jumia’s “prove it” year, and the company delivered. I am highly encouraged that Jumia will handily beat its original projections for 2025 even after the company slightly tightened the increased guidance from Q2. During the conference call, Jumia noted that early Q4 results provided the company confidence in its Q4 and full-year projections. The following table shows the evolution of Jumia’s full-year 2025 guidance.

| Category (growth % is year-over-year change) | Q4 2024 | Q2 2025 | Q3 2025 |

| Physical orders | 15% to 20% | 25% to 30% | 25% to 27% |

| GMV | 10% to 15% | 15% to 20% | 15% to 17% |

| Loss before income tax | -$70M to -$65M | -$50M to -$45M | -$55M to -$50M |

I see two main stories. Firstly, Jumia was able to project its business performance a year in advance and beat that guidance. Secondly, this ability to forecast a full year of business sets a strong precedent and foundation for the 5-year guidance the company introduced during Investor Day. Dufay explained the tweaks along the way as the result of the volatility of “operating across nine countries, each influenced by politics and macroeconomics.”

The company’s full set of objectives for 2030 are promising:

- GMV target: $2.5B to $3.0B

- Take rate expansion: +2.0 to 2.5 percentage point improvement

- Adjusted EBITDA margin: +20%

- Self-funded growth plan (no financing needed)

The take rate increase supports the adjusted EBITDA margin goal. Positive adjusted EBITDA helps to generate the cash to create a self-funded growth plan.

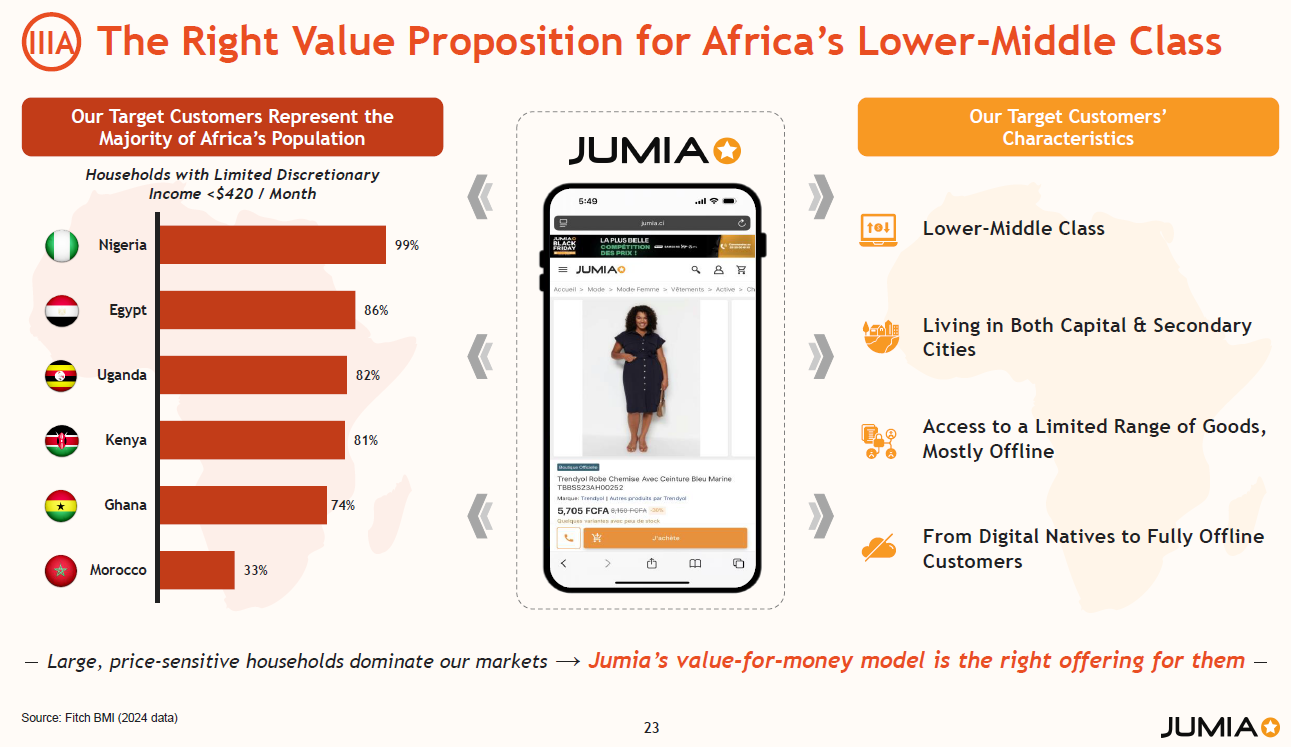

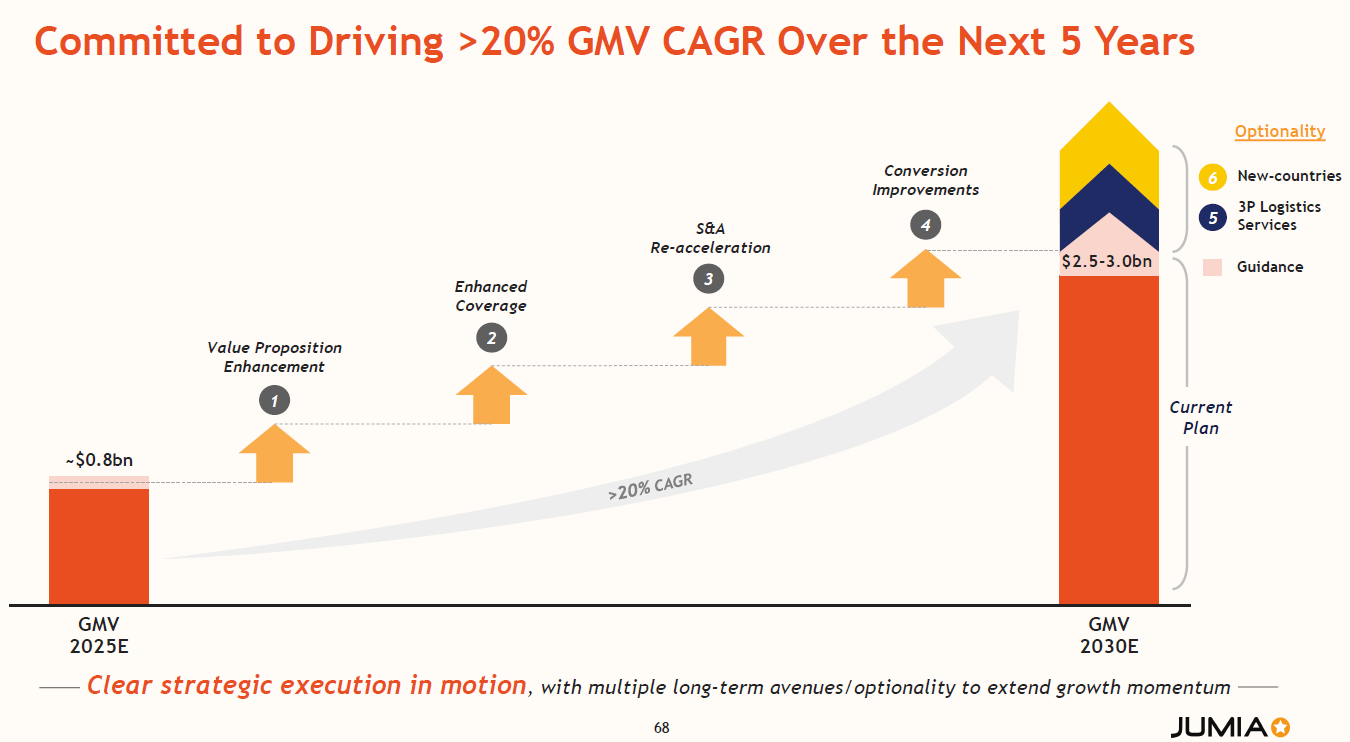

To hit the GMV target, the company needs to maintain the current growth rate over time. This scaling of the business is the core element of the company’s future success. Dufay identified “growth and scaling as the most critical factors for achieving the 2030 guidance”. He also expressed confidence in managing fixed costs and improving efficiencies. The guidance does not incorporate any growth in the annual $2K average GDP per household across Africa or expansion in the discretionary income of Jumia’s target market of lower-middle class consumers (less than $420/month per household – according to Dufay, a data point that was very difficult to estimate from available sources). The slide below from the Investor Day presentation shows that Morocco is the only country where Jumia’s target market is not the majority of the population.

The following chart from the Investor Day presentation breaks down the key drivers for GMV growth.

Of the key drivers – value proposition enhancement, enhanced coverage, selling and advertising (S&A) re-acceleration, and conversion improvements – I was least familiar with the S&A part of the business. Advertising is currently just 1% of GMV and now Jumia wants to grow this to 2% of GMV. Dufay helped me understand that the goal of increasing advertising revenue from 1% to 2% of GMV involves two main areas: performance advertising (selling sponsored products) supported by new platform tools, and campaigns paid by big brands and distributors. He explained that “scaling advertising revenue is critically linked to scale and increased competition on the marketplace”. Note that this growth in advertising will not have a negative impact on the user experience. Dufay likened some of these ads to those seen on Amazon through sponsored listings.

Increased marketplace monetization is part of Jumia’s plans to expand take rate from today’s 12.3% by an additional 2 to 2.5 percentage points in 4-5 years. I was also intrigued by Jumia’s plans for automated pricing as a part of the expansion of the take rate. Jumia will automate pricing for first-party retail products. Dufay further explained that automated pricing “is a price optimization routine that uses automated competitor checks and live sensitivity analysis to continuously optimize margins and sales, unlike the current manual pricing processes” currently in place. Implementation of this technology will continue a modernization and rationalization of the company’s tech stack that has also introduced new social marketing and seller tools and substantially reduced costs. Year-over-year Technology & Content (T&C) spend dropped from $12.9M to $8.7M. Fixed tech costs are down 10% year-over-year.

Guidance Optionality

Dufay confirmed that the optionality described in the guidance is additive.

The 3P (third-party) logistics is a $50B+ market. If Jumia exercises this optionality, the company will be able to fill routes, lift drop density (number of deliveries per route), lower fulfillment costs per order with minimal S&A, monetize existing networks, and increase coverage.

The additional countries are Angola and Tanzania, representing a combined population of 107M and $187B in GDP. Jumia has several gates before attempting to enter either country, the most important of which from my perspective is sufficient cash. Dufay explained that if Jumia entered either country before 2030, “it would require unforeseen good circumstances, such as being ahead of target and having more cash than expected”. He continued to explain that “those countries would initially require investment and take a few years to become profitable”. Other gating factors explained during Investor Day are currency stability, partner density thresholds, a seller pipeline, readiness, and payback within internal thresholds.

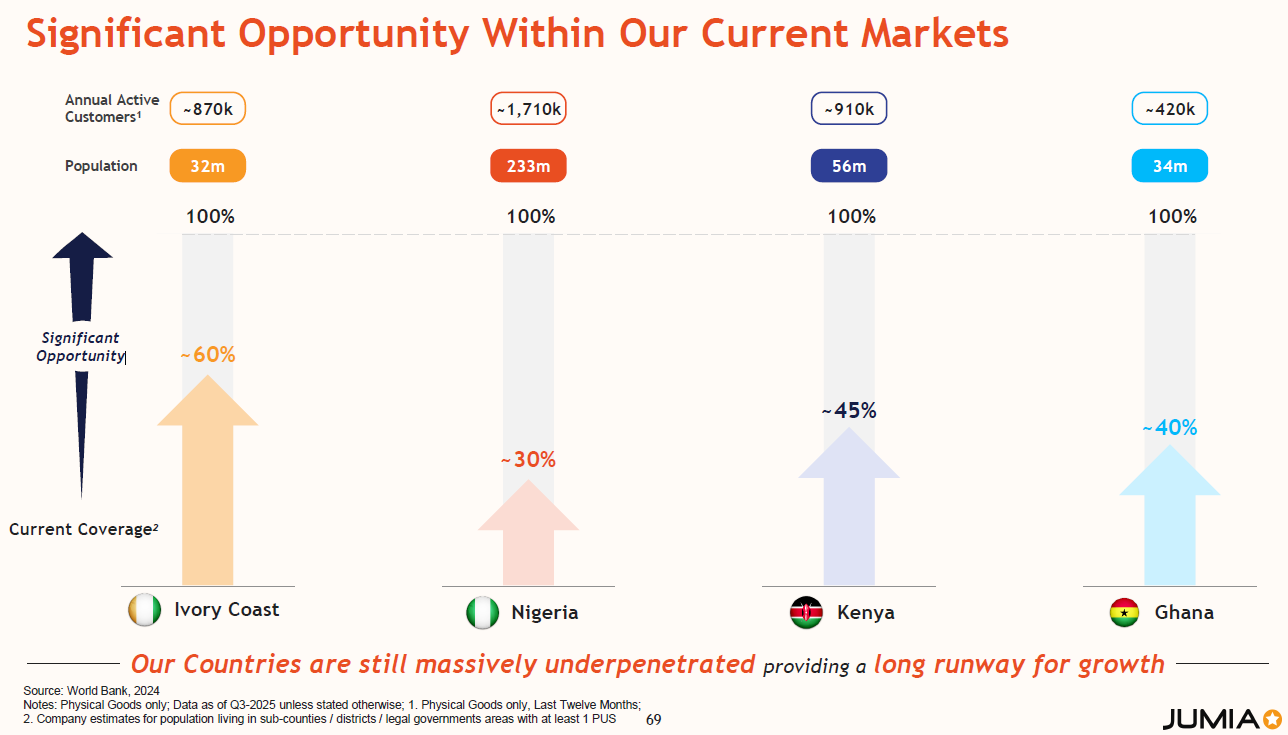

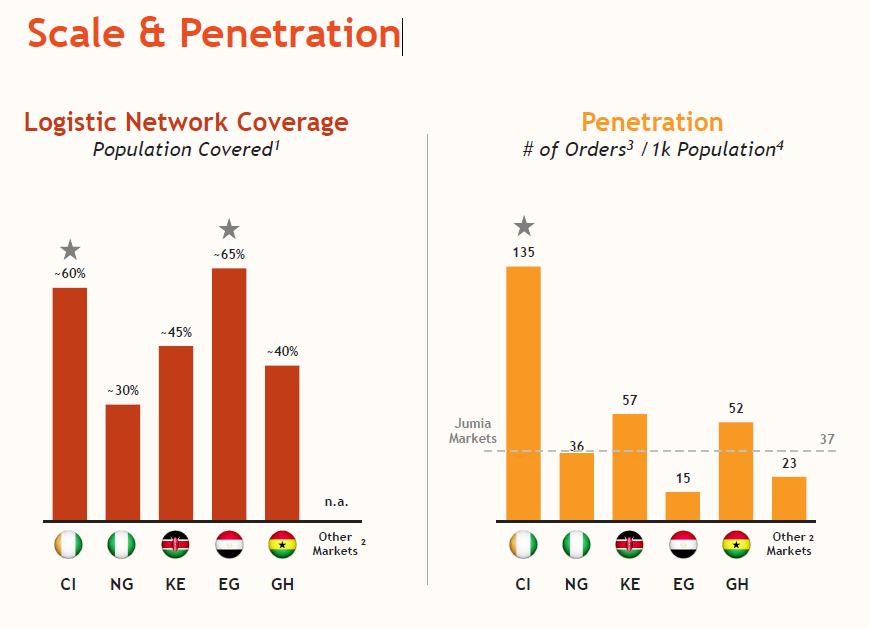

Ahead of any country-level expansion, Jumia still has plenty of opportunity in its existing countries. The charts below quantify the opportunity in terms of current coverage in existing markets and show the country-specific scale and penetration. Jumia described its markets as “massively under-penetrated”.

Jumia’s up-country expansion (outside the major urban centers) is an important part of increasing coverage. This expansion has driven some of the fastest growth in the business with “hundreds of cities” joining Jumia’s reach. Up-country orders now constitute 60% of Jumia’s business, up from 54% a year ago. Nigeria has been particularly successful in expanding beyond the major cities; this expansion is in its early stages having started about a year and a half ago.

Country-Specific Growth

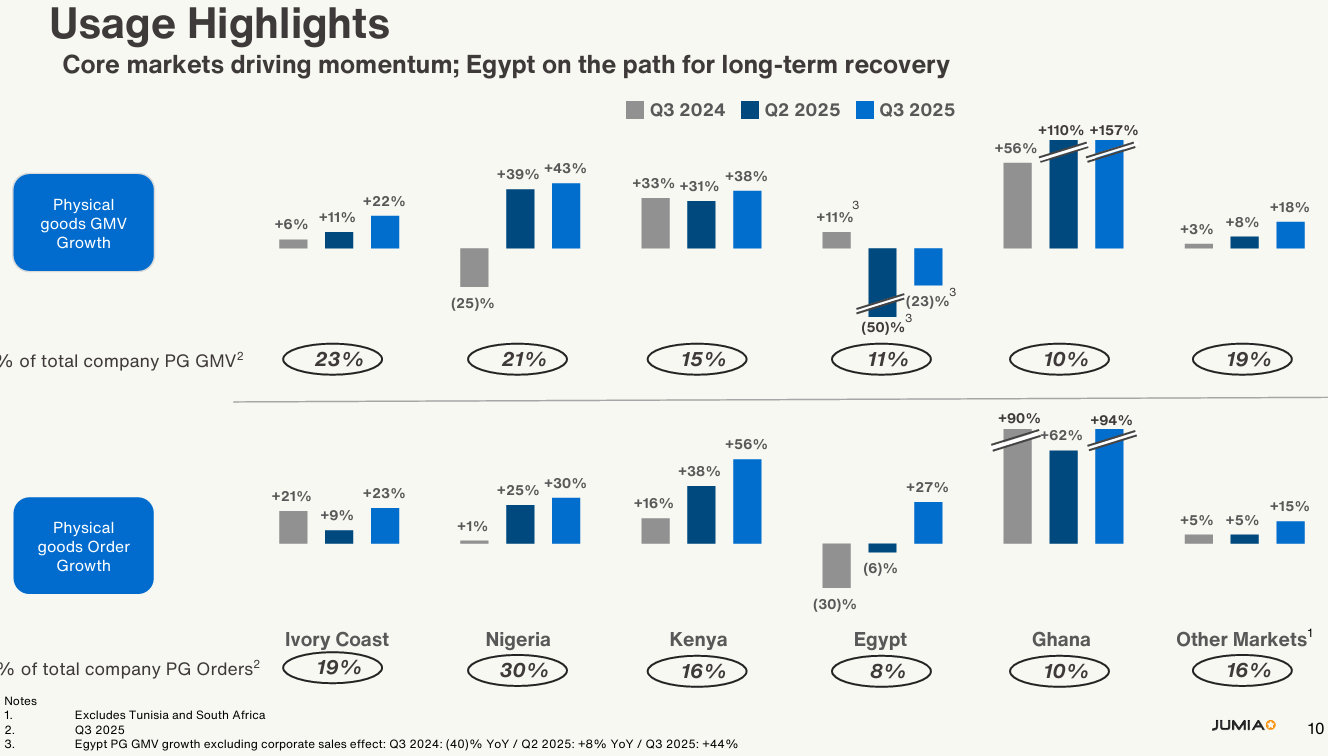

The increased visibility on country-specific market dynamics provides more evidence of Jumia’s confidence in its business. For example, in physical goods, Nigerian orders grew 30% and GMV increased 43% year-over-year. Nigeria now represents 21% of Jumia’s physical goods GMV and 30% of physical goods orders.

The country-specific metrics were strong across the board with Egypt still in recovery and Ghana continuing its extremely robust growth.

Jumia continues to introduce new services and products that it first tests in a specific country. In Q3, launched Jumia Instant in Kenya. This small pilot started in Nairobi as a service to deliver anything in the warehouse to anyone in the city in 4 hours. Jumia is looking to compete against quick commerce and to provide more convenience to those customers who are willing to pay for such convenience. The company is seeing early traction and will scale the service if it becomes successful.

Competition

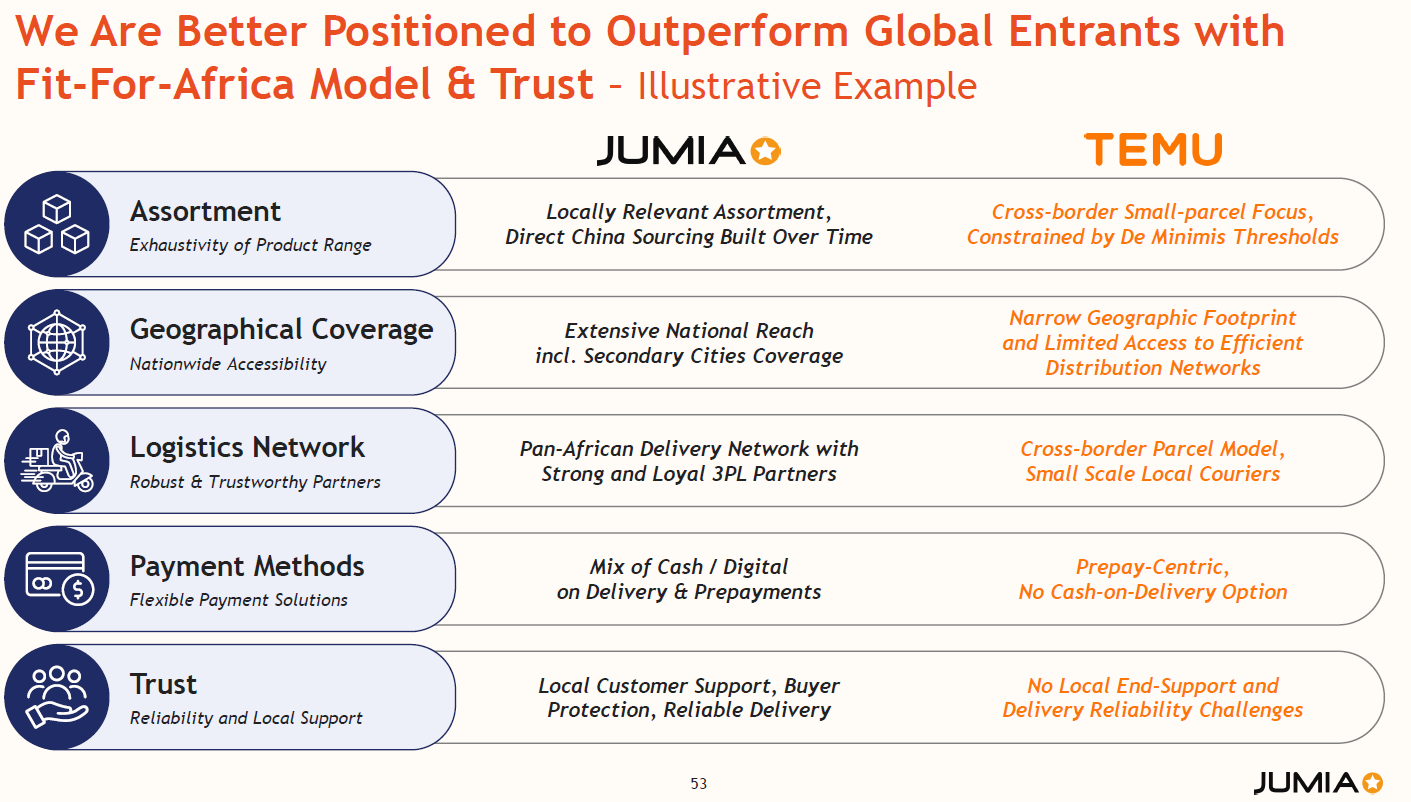

Dufay claimed that competition is not on the list of growth risks because competitors have so far been unable to scale their offerings. The company has even observed competitors reducing investments in marketing. Jumia compared itself to Temu as an example of its competitive success.

The company first provided substantial quantification of its competitiveness during its Q2 earnings report, and my related interview with Dufay.

During Investor Day, Temidayo Ojo, CEO of Jumia Nigeria, added that Temu cannot compete on higher valued items. Jumia has built local supply and can ship in a timely fashion. Moreover, the company has heavily invested in its supply chain and as a result can match Temu on price and even deliver items like fashion faster than Temu. Still, Jumia views competition positively; market pressure keeps the company “on its toes”.

Jumia’s ongoing successes with customer retention and customer satisfaction also bode well for the company’s competitiveness. In Q4, Jumia’s NPS (net promoter score) score increased year-over-year from 63 to 64. Forty-three percent of new customers in Q2 2025 made another purchase within the next 90 days. This retention metric was 40% a year earlier. Overall, orders grew 34% year-over-year, and quarterly active customers ordering physical goods grew 23% year-over-year.

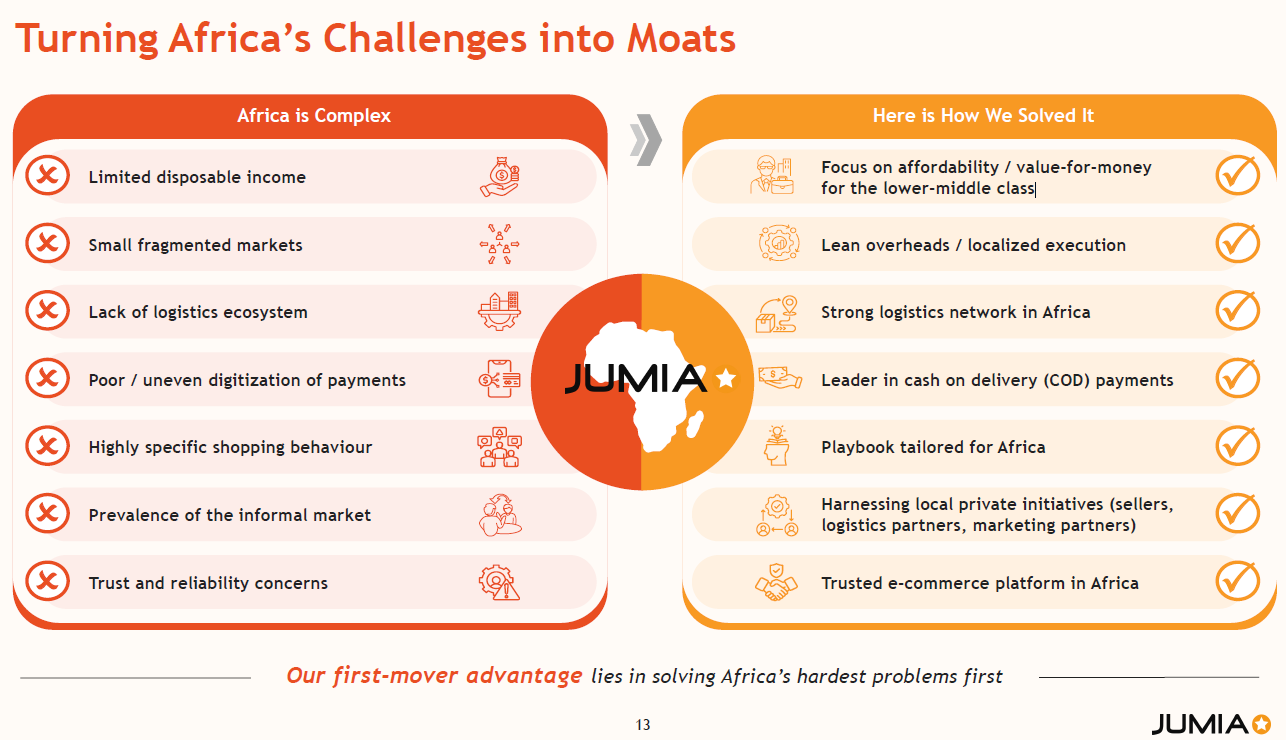

The slide below summarizes Jumia’s competitiveness in the form of transforming the familiar challenges of operating in African markets to Jumia’s unique position in solving and mitigating these challenges.

Cost Reductions

As the slide above shows, Jumia’s ability to continue driving fulfillment costs lower is a part of the company’s expanding moat. Lower costs contribute to affordability and value-for-money for Jumia’s market of lower-middle class customers. Cost reductions and efficiencies have also been a key part of Jumia’s turnaround on the way to eventual profitability.

Jumia reduced its average fulfillment expense from $3.5 to $2.1 per order over the past 3 years, a 40% drop. For 2030, Jumia is estimating a reduction to the range $1.3 to $1.5. Thus, in the next 5 years, Jumia will achieve at most the same percentage improvement it achieved in the prior years. Dufay explained that “the rapid initial decrease [came from] cutting very fat low-hanging fruits or significant waste in the supply chain”. He further explained that while “scale effect and optimization are the main drivers” of future improvements, “some mix effects, such as scaling the supply from China (mostly small and light items), will also help with efficiency numbers”.

The following narrative from Investor Day provides rich color on Jumia’s major achievement in simplifying the business and reducing costs (approximately quoted):

“A fulfillment reset is driving lower unit costs. Core to changes. Changed everything. Redefined and redesigned the service level agreements. Shifted most deliveries from door delivery to pick-up stations. Finally could deliver a service customers are willing to pay for. Massively simplified the business and saved money for customers. Adjusted service level to what people are willing to pay for”.

Partnerships and Major Investors

During Investor Day, an analyst asked Jumia about its partnership with pan-African telecommunications group Axian Telecom. The company made a major (8%) investment in JMIA and nudged its stake right to the edge of 10% above which the SEC would consider the company an insider and require additional regulatory oversight and disclosure. This substantial support even created rumors of potential buyout interest. Thus, understandably, expectations are likely building for some explicit relationship beyond the board position taken by an Axian representative. Jumia noted a laundry list of potential business opportunities and synergies like Axian products sold with Jumia, BNPL (buy now, pay later) services, overdraft and financing for SMEs (Small and Medium-sized Enterprises), connectivity and internet in warehouses. The main opportunity with Axian is fintech for consumer finance. However, at this time, Jumia is not ready to disclose anything “tangible”. In our discussion, Dufay cautiously noted that expectations are low for now because Jumia is not currently prioritizing fintech.

Ahead of earnings last week news arrived of another major investor: Pleasant Lake Partners LLC stepped up and purchased a 7.83% stake in JMIA. According to Dufay, this investment ushers JMIA into “a new world of investors with billions of dollars in assets under management (AUM)”. Importantly, this attention allows JMIA to “engage with bigger, non-specialized funds who are familiar with emerging market stories”. Dufay added these investors can “see the upside in Jumia’s model”.

These major investors are also providing a base of support for Jumia’s stock which will be useful as the company focuses on achieving its long-term growth plans cutting across quarter-by-quarter volatility.

Starlink

Jumia still has a nascent partnership with Starlink. Dufay confirmed that Starlink sales are performing well, but are not yet a material part of the business. Once Starlink grows to a material part of the business, I expect synergistic effects of expanded internet access providing another driver of growth for Jumia. In the meantime, Dufay said Jumia is “unable to disclose specific numbers”. During Investor Day, the company mentioned Starlink is sold in 3 countries with a 4th coming. Ivory Coast is likely the next market given the current wrangling over regulations around the sale and use of Starlink in the country.

Valuation

All this good news begs the question: is JMIA already priced for this potential success? I do not think so, but the stock is not currently the “steal of a deal” that it once was.

JMIA is up over 165% year-to-date and trading at almost 6 times its value from the April lows. I have consistently bought into the opportunities the market has offered and presented strong buy ratings the entire way. Now, JMIA is no longer priced at a discount to the risks inherent to the business. The stock’s valuation of 6.7 times trailing twelve month (TTM) sales and 6.0 times forward sales makes it more or less fairly valued for the very near-term. However, relative to the future long-term opportunity, I consider JMIA shares priced low enough for a buy recommendation. So while I am stepping down from the strong buy rating, I consider this action a “recalibration” and not a downgrade. I am just as bullish as ever on Jumia’s prospects, but the “physics” of valuation require me to place a buy rating at this juncture. If the market offers steep discounts in the future, I will of course dutifully upgrade to a strong buy.

The 2030 guidance provides an approximate starting point for creating a long-term valuation metric. GMV at $2.5B, a take rate of 14.1%, and an adjusted EBITDA margin of 20% provides approximately $70.5M in adjusted EBITDA. Assuming 122.46M shares outstanding for the next 5 years, the stock would earn $0.58 per share in adjusted EBITDA. With Jumia’s stock trading around $9.65/share at the time of writing, this calculation implies a 16.6 price/earnings ratio (again, using adjusted EBITDA as the proxy for earnings). At the upper-end of Jumia’s guidance, the company would earn $0.71 per share in adjusted EBITDA for a 13.6 P/E. For a very rough comparison, the market values Latin American e-commerce company MercadoLibre, Inc (MELI) at an extremely lofty 28.5 EV/EBITDA (EV = enterprise value). Thus, JMIA is likely trading at an attractive discount to its potential long-term valuation. At a 28.5 P/E, JMIA would trade somewhere in the range of $16.5 to $20.2.

Conclusion

The path to achieving 2030 guidance will not be smooth. The volatility in African markets and politics nearly guarantees that Jumia will experience bumps in its plan. Those moments will offer long-term investors buy-the-dip opportunities. In the meantime, the stock is acting like it is in wait-and-see mode on the long-term guidance. The stock dropped 4.0% after earnings, and a sharp rebound in the wake of Investor Day was just as quickly faded. The trading since then has been choppy and tepid partially thanks to a weakening stock market.

From a technical standpoint the stock is also vulnerable to a growing downtrend from its 20-day moving average (DMA) (the dashed line above). Moreover, the stock is now trading below the 50DMA trendline (the red line above) that supported a tremendous recovery from the April lows. I am fully expecting a period of “consolidation” where the stock will “digest” its recent gains and get buffeted by exogenous stock market and financial market pressures. If the stock trades to $8.50 or lower, I will add to my shares…all else being equal.

Be careful out there!

Extensive article on Jumia from Hunterbrook: https://hntrbrk.com/jumia/