The SaaSpocalypse, or what I sometimes generally call the AI Panic, is a watershed investing event. Whole fortunes are stumbling down a path of destruction in this moment. Yet, the survivors of this indiscriminate selling will yield tremendous returns in coming years. Panic does not distinguish between fragile business models and structurally durable platforms. In periods of indiscriminate selling, valuation compression can dramatically overshoot structural risk.

As a trader and investor who focuses on market extremes (like the market breadth trading rules), I seek durability despite the noise. My goal is to understand whether AI represents an abstraction layer, a structural value shift, or a software extinction event. In this post, I apply a structured analytical framework to Atlassian (TEAM) to test whether the market’s collapse narrative holds up under scrutiny.

I have previously examined individual cases in the SaaSpocalypse – “A Thoma Bravo Lens On Sorting SaaSpocalypse Survivors” and “BOX Caught in an AI-Driven Software Selloff: Identifying Platform Opportunities Amid Market Fear” – but this post is the first time I apply my comprehensive durability framework to a single company in depth.

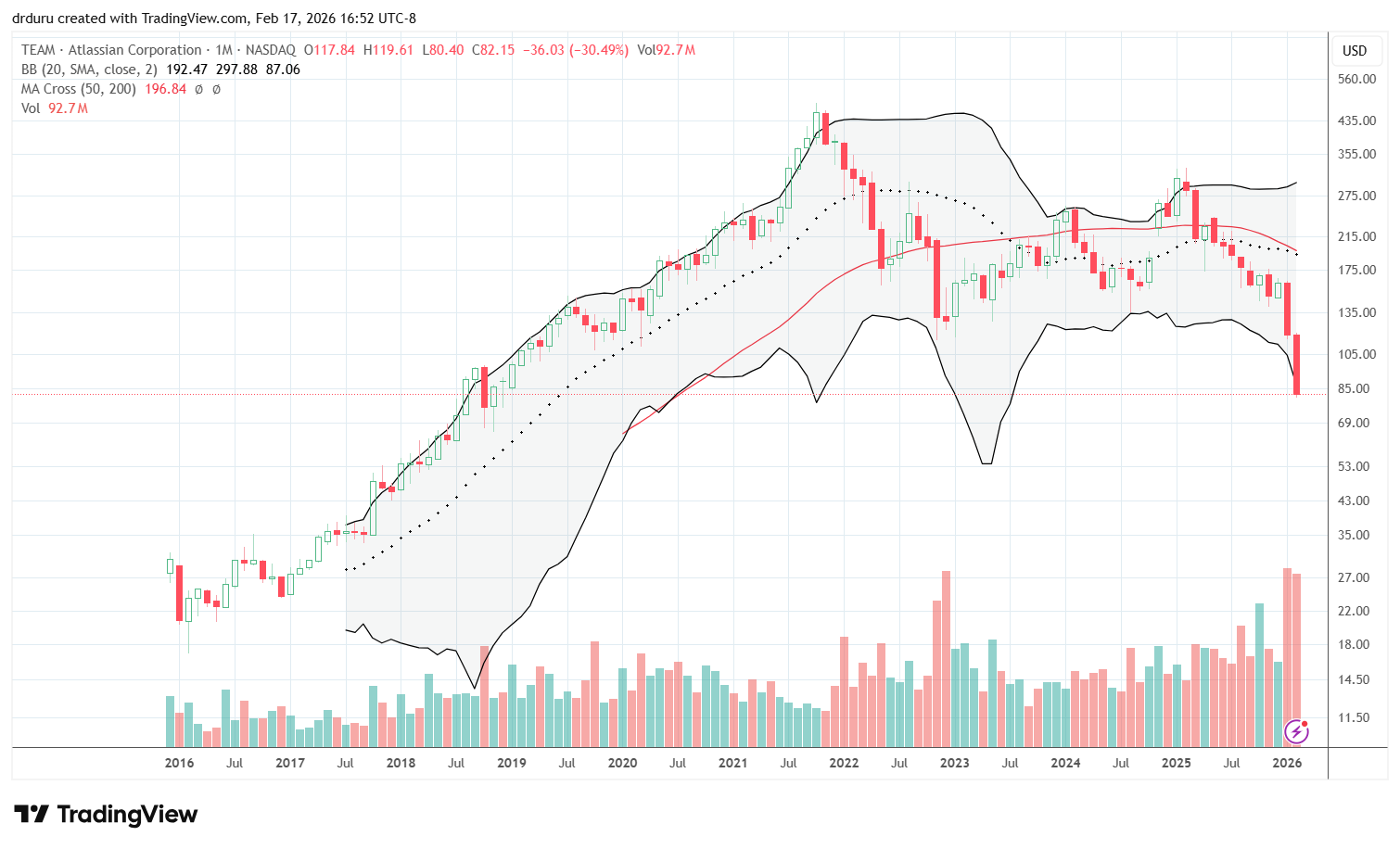

TEAM: A Collapsing Stock

While I am convinced Atlassian is positioned to survive the Saaspocalypse, the market is thoroughly convinced otherwise. TEAM even peaked ahead of the generative AI onslaught. The stock hit a stratospheric all-time high along with so many other tech stocks in the pandemic-aided tech bubble of 2020 to 2021; TEAM may never revisit its $458 closing all-time high. Yet, with a gut-wrenching 49% loss in the first 6 weeks of 2026 and a 7+ year low, the stock looks like a steal that just keeps getting ever cheaper. The panic and indiscriminate selling is now so intense, there is no clear bottom in sight for TEAM and similar victims.

Thus, while I have initiated a position in TEAM, I am pausing before adding more shares at lower prices. The monthly chart below shows the stark nature of TEAM’s price destruction: 83% off its all-time high yet still up almost 5x from its 2016 lows (similar to the NASDAQ’s 5.3x gain in that same time).

Introduction to the Structured Analysis

I have used Atlassian’s various software products for many years, and I have struggled to imagine a world where Atlassian is disintermediated by AI-first tooling. I particularly like Confluence and its AI-driven knowledge management capabilities. So when I got an email today announcing “Discover powerful ways to start using Rovo AI”, I decided to run TEAM through my SaaSpocalypse analytical framework. The results are compelling: Atlassian is poised to survive the SaaSpocalypse, and TEAM is priced low enough to offer significant future returns at the other end of the AI Panic.

In its Q2 2026 earnings report, Atlassian reported accelerating cloud momentum and a rapidly scaling AI layer using Rovo. In a market where “AI will eat software” is now the clarion call for panic, Atlassian’s results deliver concrete and quantifiable evidence that AI can increase enterprise software usage and monetization.

The rest of this post uses ChatGPT to help analyze Atlassian’s results as communicated in the transcript from the conference call. The analysis is based on my synthesized SaaSpocalypse framework. I have also provided more context from the earnings report, shareholder letter, and valuation metrics and conclude with my final thoughts.

This post does three things:

- Integrates Atlassian’s Rovo metrics into the framework analysis.

- Extracts other high-signal AI points from management and analyst Q&A.

- Draws conclusions about Atlassian’s ability to survive the SaaSpocalypse.

The Objective and the Framework

This exercise systematically tests whether AI will destroy Atlassian’s economic engine or strengthen it. In every analysis like this one I ask the following: is AI primarily (A) another abstraction layer, (B) a structural value shift, or (C) a software extinction event?

For consistency across analyses, I apply a scoring overlay designed to test competing narratives:

Competing narratives

- Levie thesis (platform/context/guardrails): AI increases the value of platforms that own context and can enforce permissioning, governance, and safe execution inside workflows.

- O’Laughlin thesis (memory hierarchy/API): value migrates away from human UI and toward “source-of-truth” layers, APIs, and infrastructure-like persistence; some UI-centric software becomes vulnerable.

- Software Dead? Nah overlay: disruption timelines are long and uneven; AI increases total software volume; value shifts by layer; domain depth becomes more important.

A central test cutting across these narratives is the Jevons Paradox. When the cost of cognition falls, does total software usage expand or contract? If AI lowers friction and increases the number of work objects, coordination requirements, and governance needs, software platforms benefit from expansion. If AI substitutes away coordination and collapses the need for structured workflows, value capture erodes. Every company in the SaaSpocalypse can be judged on which side of this expansion–substitution divide it falls.

For each company/event, I score the following categories:

- Context ownership (Strong / Medium / Weak)

- Governance & guardrails (Strong / Medium / Weak)

- Agent orchestration capability (Strong / Medium / Weak)

- Economic alignment (Strong / Medium / Weak)

- Substitution resistance (High / Medium / Low)

- Domain depth amplification (Strong / Medium / Weak)

- Software volume signal (Expanding / Neutral / Contracting)

- Timeline signal (Short-term substitution / Coexistence / Long-term expansion)

Rovo and Key AI metrics

Atlassian’s CEO opened with a set of AI datapoints that are convincingly operational:

- “Rovo surpassed 5 million monthly active users of our AI capabilities.”

This data point matters because Atlassian is claiming meaningful scale in active usage. AI enablement is increasing Jira activity.

“When we look at the thousands of customers in our software teams using AI code generation tools, we found that they create 5% more tasks with Jira, have 5% higher monthly active users and expand their Jira seats 5% faster than those who don’t use these AI coding tools.”

This claim is the clearest “AI increases software volume” statement. AI does not merely make developers faster. Developer productivity turns into more throughput, which turns into more work objects (tasks/issues) and more coordination, which increases demand for a system of record for work.

Michael Cannon-Brookes, Co-Founder, CEO & Director, explained the logic as follows:

- “…that innovation moving quicker, it doesn’t mean you’re finishing your road map. You’re coming up with more things to do. So you’re adding more tasks”.

- “More software in the world is a good thing for Atlassian. I think we’ve said that for a couple of years now”.

- “That is our belief that AI is unlocking sort of human creativity at the highest level…It’s allowing them to create more. That means those humans have to interact and collaborate more and those created objects need to be managed, operated, maintained and that’s generalized a good thing for Atlassian across software and non-software teams”.

“Context” and “guardrails” spelled out as a product asset

Atlassian’s claims align directly with Levie-style platform/context/guardrails:

- “…the data and domain expertise living inside our Teamwork Graph, which is now well more than 100 billion objects and connections across first and third-party tools, enables Rovo to deliver real business value that’s context aware and actionable for customers across their search, chat and agentic experiences…”

- “…our decade-long investments in enterprise-grade security, data governance, permissioning capabilities and compliance enable every organization to securely move work forward at scale while deploying these fantastic new AI capabilities with the trust that they need. We provide a system of work built on deep integration into customer workflows with that compliance, security and support that enterprises trust built in”.

These claims define:

- Context ownership (Teamwork Graph scale + cross-tool connections)

- Governance & guardrails (permissioning, compliance, enterprise security)

AI monetization: Teamwork Collection seats and credits

Atlassian also pointed to its driver of AI-based monetization:

- “In less than 3 quarters, more than 1,000 customers have upgraded to our main AI monetization driver, the Teamwork Collection, purchasing more than 1 million seats to get the best AI platform and many more AI credits for their agents”.

In other words, AI drives seat upgrades plus incremental credits.

Benefiting from the Jevons Paradox

The company said AI tool usage correlates with more tasks, higher MAU, and faster seat expansion in Jira. The evidence directly demonstrates Jevons-type expansion in measurable workflow objects.

- Lower friction → more throughput

- More throughput → more work objects + more complexity

- More complexity → more coordination and governance needs

- Those needs increase demand for the work system-of-record (Jira/Jira Service Management/Confluence) and the AI layer embedded within it (Rovo)

1) Context ownership: Strong

Atlassian explicitly anchored Rovo’s differentiation in the Teamwork Graph with “well more than 100 billion objects and connections across first and third-party tools…” Atlassian has operationalized the context that agents need to work effectively. This context includes a large graph of work objects and relationships. Teamwork Graph is a comprehensive knowledge management layer.

2) Governance & guardrails: Strong

Management emphasized security, governance, permissioning, and compliance as decade-long assets. However, the company did not provide details on audit or budget control mechanics at the agent level (e.g., per-agent logs, policy simulation, spend caps). I will be watching for more information on such mechanics in the future.

3) Agent orchestration capability: Strong

The call repeatedly referenced agents running inside workflows at scale. For example, the company claimed its customers now run AI agents in millions of workflows per month. Thus, the platform is orchestrating at scale.

4) Economic alignment: Strong

Per the monetization referenced earlier, Atlassian presented a monetization pathway already in motion (Teamwork Collection upgrades, AI credits, long-term commitments). When analysts pressed for a timeframe for monetization, management responded by pointing to evidence in forward indicators:

- “Our RPO [remaining performance obligations] number has ticked up for the third quarter in a row and is growing significantly faster than our Cloud revenue growth and the Cloud revenue growth also accelerated this quarter”.

In Jevons terms: if AI increases work objects and collaboration needs, Atlassian benefits when monetization is tied to seats + packaged AI + overage credits.

5) Substitution resistance: High

Atlassian’s Jira remains the human and process anchor for work, a control-plane argument. Cannon-Brookes made the point succinctly:

- “Customers don’t use models, they use applications… we don’t sell chips, we sell apps. And those apps have to deliver value and those models let us deliver better value”.

- “…you can model your business process in Jira, you can model your workflow in Jira, and you can involve other agents from your agent platform of choice or as most enterprises will probably end up with multiple agent platforms, and we have an out-of-the-box offering that works for you…”

These claims imply that Atlassian has positioned Jira as the workflow substrate where humans, approvals, and processes remain well integrated even with external agents.

6) Domain depth amplification: Strong

Atlassian pointed to broad expansion into business workflows, especially in its Service Collection (HR, finance, customer service), and the company tied agentic adoption directly to Service:

- “In the last 6 months, more than 40% of the Agentic workflows… are actually in Service Collection customers and Service Workflows.”

- “More than 2/3 of our service collection customers are using it for non-IT use cases…”

This domain depth demonstrates AI embedded into specific operational domains.

7) Software volume signal: Expanding

For Atlassian, AI increases throughput and complexity. The complexity increases the need for coordination and tracking work: “…you create more complexity… more technology… you end up with more collaboration to do…” Moreover, with 5% more tasks in Jira and 5% higher monthly active users, customers expand Jira seats 5% faster.

8) Timeline signal: Coexistence → long-term expansion

Nothing in the call suggested near-term substitution where agents eliminate Jira/Confluence. The company framed a long-lived coexistence: external agents will exist, but Atlassian remains the process anchor and the source for context.

Answering Analyst Skittishness

Unsurprisingly, analysts grilled management in an effort to assuage their concerns about Atlassian’s durability in the SaaSpocalypse. Analysts pressed management on three issues: pricing durability, competitive displacement by Anthropic, and model switching risk.

Pricing: Atlassian rejects “seat-based is doomed” (and argues AI costs are well-managed within the platform)

An analyst asked the question the market is obsessing over: seat-based pricing versus consumption. Cannon-Brookes started his answer with a staunch defense of the company’s pricing model and customer retention (emphasis mine):

“You can see in everything from the RPO to our NRR number, again, 120% ticking up for the third quarter and 120% plus, north of 120% and ticking up for the third quarter in a row. The pricing we currently have is delivering, right, for the customers. They are opting for more of what we are doing.”

The CEO went on to explain the company’s philosophy which helps customers directly control costs, including AI-driven costs:

“It is our job, I believe, as an application vendor, not an infrastructure vendor, but an application vendor, a platform vendor to manage the costs of everything that we have in the envelope of what the customers pay. We’ve done that in storage. We’ve done that in network costs. We’re now doing it in AI costs.”

Atlassian’s customers prefer the pricing predictability that comes from the seat-based model. As a proof point of success, Atlassian has delivered its 5 million Rovo seats while improving gross margin at the same time. AI can be bundled predictably in seats while costs are managed internally. Atlassian is explicitly pushing back on the idea that usage must be priced purely as metered consumption.

Atlassian reframes competitive risk from Anthropic Cowork as integration leverage, not displacement

A frustrated analyst asked about the competitive risk from Anthropic Cowork after framing his question in the context of a stock falling another 10% in the after-hours despite all the good news from the earnings report.

Cannon-Brookes answered in three parts:

- Anthropic is a partner: “We use a lot of their models…”

- These new tools still need context and data: “They continue to require places to exchange”.

- Atlassian is exposing access via MCP: “One of the greatest uses of our MCP server, as an example, is a way to get to Atlassian’s offering and the Teamwork Graph and the context we have in those other tools is through things like Cowork and use of Atlassian’s MCP server. That is really good for us…”

Atlassian has a control-plane strategy. The company is the governed context layer and workflow substrate even when an external agent is the interface. The software suite is not threatened by “UI extinction”. Atlassian allows external interfaces while keeping Atlassian’s graph and workflow state as the enduring layer.

How Atlassian wins even with model switching

An analyst asked about developers switching between coding models and agents. Cannon-Brookes pointed out that the company itself uses models from multiple foundation labs “within the customers’ preferences and choices” and customers may not even notice the switching:

“We have a very good AI team, world-class in adopting new models, working out where they’re stronger, where they’re cheaper, where they’re faster, where they deliver better quality results and getting those into our products really quickly”.

Cannon-Brookes further emphasized a 20-year old approach of solving human problems not technology problems: “Jira is about the human reference to work”. Thus, Atlassian leans on AI as an abstraction layer. Models change rapidly, but apps and workflows persist. The company is flexible and durable by being model-agnostic.

Can Atlassian Survive the AI Panic?

While the selling in the shares says Atlassian will not survive (or at least suffer mightily), the current evidence suggests survivability, not structural impairment. The business model, the technological capabilities, and the customer-orientation all point to a company built for the SaaSpocalypse. In summary:

- Teamwork Graph as context moat (100B+ objects/connections)

- Governance/permissioning/compliance as an enterprise “agent safety” moat

- Monetization pathway already scaling (Teamwork Collection: 1,000 customers, 1M seats; Rovo 5M MAU)

- Interoperability/control-plane posture (MCP + “workflow substrate” positioning)

Price and valuation signals

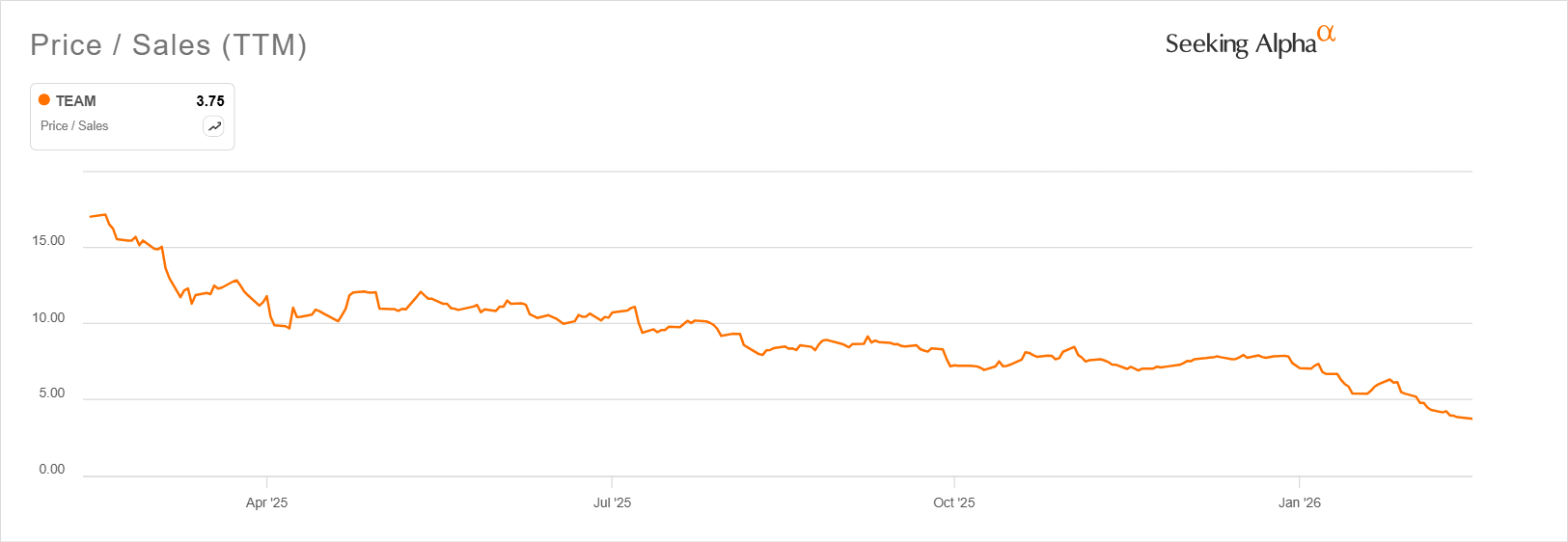

The current price spiral in TEAM reflects a rapid rerating of the stock in a sector suffering rapid valuation compression. For example, at the same time TEAM’s price/sales ratio has plunged from double digits to single digits, the stock remains just above the sector median. The discount is not obvious from comparing to peer multiples; it becomes clear when contrasted with Atlassian’s AI adoption signals, retention/commitment indicators, and control-plane positioning.

TEAM has quickly fallen from a premium priced software stock to the kind of value stock that acquirers like Thoma Bravo love to take private. TEAM’s forward PEG ratio (price/earnings divided earnings growth) is even below 1.0 now (on a non-GAAP basis).

Backing confidence with action

Atlassian’s shareholder letter starts with the CEO’s clarion call for calm and confidence. Cannon-Brookes declared that “we had a fantastic Q2”, and “we’re building a bloody great business”. He declared that “I’m convinced AI is great for Atlassian”. The CEO went on to refute those who think software is dead by providing financial results and customer testimonials that should cut through the noise that overwhelms nuance.

The company’s founders are backing up words with actions pausing their regularly scheduled share sales that have happened ever since the IPO. (Of course by this time their wealth from share sales should keep them comfortable well into retirement). Moreover, the company will “accelerate the pace of share repurchases in H2 relative to H1”. Atlassian repurchased more shares in January than in all of Q2.

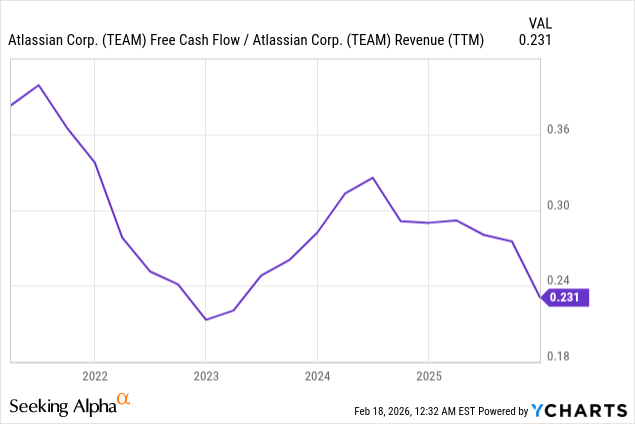

A blemish from free cash flow

This expressed confidence is important because the company’s free cash flow margin has actually been in decline since a recovery peak in 2024. Free cash flow margin is approaching lows from the 2022 bear market.

The company provided the following explanation for the current decline in free cash flow:

“Free cash flow decreased 51% driven primarily by timing differences in cash collections and tax payments, as well as higher severance and acquisition-related payments. A greater proportion of our Q2 billings landed in December this year, which will be collected in Q3. Additionally, collections growth in the quarter was impacted by our transition from upfront to annual billing on multi-year agreements, which was implemented in the second half of FY25.”

I want to see free cash flow margin bottom out at current levels to have full confidence in what I see as a significant valuation discount. On-going deterioration in free cash flow would undermine the “AI is accretive” thesis.

What Could Break The Bullish Thesis?

My bullish thesis could break upon further evidence. I will be monitoring the possibilities in coming quarters. For example, if Anthropic owns the agent layer, Microsoft owns the horizontal productivity layer, and switching costs collapse, then Atlassian could become workflow plumbing. That is, the invalidation of the bullish thesis could show up as weakening context ownership and strengthening substitution forces: the agent layer becomes the primary interface and decision layer, while Atlassian is reduced to a back-end ticketing and knowledge database with compressed pricing power.

Other potential flashpoints that would run counter to the current business dynamics include:

- Evidence that Rovo adoption stalls

- Evidence that MCP disintermediates Teamwork Graph

- Evidence that AI usage reduces seat counts

- Evidence that Service Collection fails to scale

Conclusion

I am tempted to continue dollar cost averaging into TEAM as it declines. However, I decided to stop because bear markets often disrespect analytical support levels. The energy of panicked sellers endures well past points that analytically or technically make sense. I have enough of a position in TEAM now where I am content to wait for signs of stabilization before accumulating more shares. I no longer want to argue with sellers and prefer to celebrate with buyers.

In particular, I will get incrementally more comfortable with TEAM after it fully reverses its loss from the last earnings report and closes above its post-earnings intraday high at $103. Until then, the odds remain uncomfortably high that my carefully crafted assessment becomes a speed bump on the way to much lower prices.

Going forward I will closely monitor the following fundamentals:

- Rovo MAU growth

- AI credit overages

- Service Collection seat growth

- Gross margin trend

- Free cash flow margin stabilization

If AI is an abstraction layer for Atlassian rather than an extinction event, the current pricing of the stock is panic, not prophecy.

Be careful out there!

Appendix: Methodology

I am using ChatGPT to integrate the compelling and sometimes contradictory insights of several thinkers and developers into an analytical framework. I have iterated this model over the past several weeks with my own analysis and implemented self-learning instructions for ChatGPT. Every week, ChatGPT conducts deep research looking for confirming and falsifying evidence for the framework. It also proposes updates to the framework which I in turn evaluate for integration. In a future post, I will describe this living framework in full detail.

Full disclosure: long TEAM

This was very detailed write up. And a reminder that I’m swinging these trades on very limited information and foresight lol. I’m glad we have this access to pick your brain and learn your concerns. What’s your Average price on TEAM?

It’s a learning process for us all!

My cost basis on TEAM right now is $85.85.

And just as I feared when I wrote this article, $TEAM is very much still in freefall. So I am on hold until there is some kind of signal, technical or fundamental, that convinces me to start buying again. Stay tuned….

Perhaps I could offer you a book to read. “…Of Mice and Men”

January/February forced me into daily Momentum trades. End of day I am out of the market or into Sgov

@Richard – that’s an interesting recommendation! I cheated and asked AI why would someone who read this post recommend reading this book. I got an article-sized explanation with the following introduction: “A reader likely recommended Of Mice and Men because your article centers on conviction in a fragile moment — optimism in the face of collapse — and Steinbeck’s novella is fundamentally about the tension between vision and harsh reality.”

This book is of course a classic and now I have even more reason to finally read it!

Fascinating approach to trading. I take it you find this day trading approach to be a way to preserve capital?