Jumia Technologies (JMIA) reported strong Q4 2025 results. At the same time, the company is entering another important phase in its development as scale and economics align more visibly within the business model.

On a year-over-year basis:

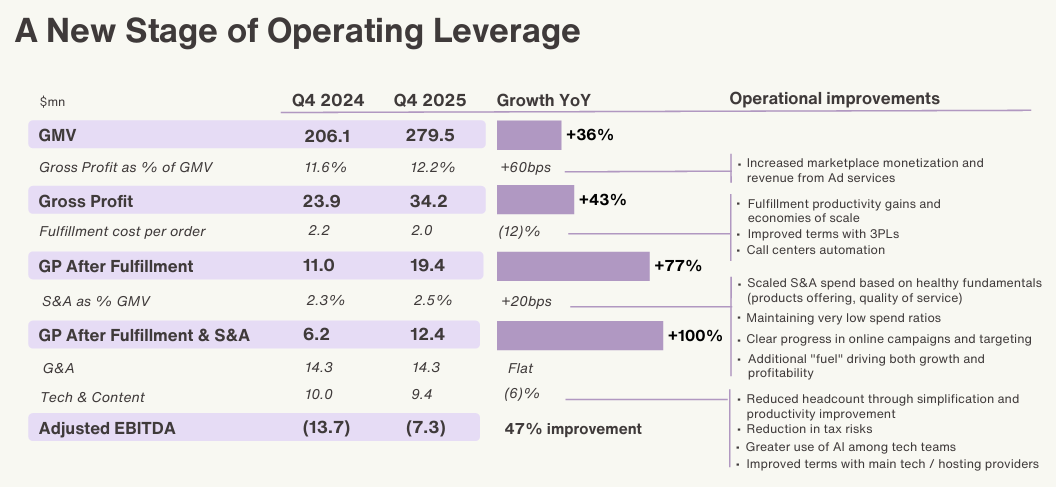

- GMV +36%, with physical goods GMV +38% (adjusted for the exit from Algeria)

- Physical goods orders +32%

- Quarterly active customers +26%

- Revenue +34% to $61.4M

- Gross profit as % of GMV increased from 11.6% to 12.2%

- Gross profit +43% to $34.2M

- Gross profit after fulfillment +77%

- Adjusted EBITDA loss narrowed to $7.3M from $13.7M

The headline numbers are strong, but the more important development is structural.

Operating Leverage Takes Center Stage

In my quarterly earnings interview, CEO Francis Dufay emphasized the significance of what the earnings presentation described as a “new stage of operating leverage.” He called this development “really important,” explaining that “the combination of growth and operating leverage has massive impact all the way down to the [adjusted] EBITDA.”

The dynamic is straightforward. Continued growth in GMV is now accompanied by accelerating gross profit growth and meaningful improvement in gross profit after fulfillment and S&A. At the same time, fulfillment cost per order continues to decline. Recent commission increases have contributed to take-rate expansion, reinforcing the link between growth and margin.

As Dufay described it, operating leverage is “working.” He framed the current position as one in which Jumia has achieved product-market fit and is “in the right place at the right time.” The emphasis throughout our discussion was not on growth alone, but on growth translating into improved economics.

Growth With Monetization and Discipline

Jumia guided to 27% to 32% GMV growth in 2026. While falling just short of elevated market expectations, Dufay described the range as “a complicated but necessary balance between growth and monetization…intended to be achieved while simultaneously increasing vendor commissions, retail monetization, and advertising monetization.” The company remains focused on avoiding “chasing growth for the sake of it.”

On the earnings conference call, he characterized the guidance as “hopefully a bit conservative,” assuming a stable macro environment. The consistent message across both the interview and the call was that scale should enhance margins rather than dilute them. The objective is not simply volume expansion, but disciplined monetization layered onto growth.

Capacity, Infrastructure, and the Playbook

Operating leverage requires infrastructure that can support higher volumes without proportional increases in investment. On the conference call, Dufay stated, “We believe we are in the right place for the next two years with our current capex. The tech platform is the right stack to manage three times the volume.” While some markets, including Ghana, may require warehouse expansion in 2027, the current footprint will support continued scaling. For example, the company continues to expand upcountry with 61% of order now coming from these regions versus 56% a year ago.

In our discussion, Dufay described how operational efficiencies are embedded in the model: “Reverse logistics is fully embedded in the routing. Trucks drop forward packages and pick up reverse packages in the same run.” Management continues to target improvements in cost per package as warehouse management systems mature and scale efficiencies deepen. Fulfillment cost per order declined 12% year-over-year to $1.97 (declined 20% in constant currency terms), reinforcing the link between volume growth and unit cost improvement.

Ghana provides a clear example of the company’s execution framework in action. Q4 results showed physical goods orders up 82% and physical goods GMV up 124%. Dufay credited a strong local team that quickly adopted the updated plan introduced in 2023. He observed that when a country executes correctly, business “keeps getting better,” and described Ghana’s performance as the result of “the same playbook” used in Ivory Coast, Senegal, Kenya, and Nigeria. “Ghana is a sizable market with similar potential,” he noted, adding that expansion into northern cities provides additional room for growth and that online competition remains limited.

Product-Market Fit and Order Economics

Appliances were highlighted as a Q4 growth driver. In our interview, Dufay explained, “Appliances is an amazing category for us…appliances have been the best category for us in Ivory Coast since 2014.” Affordable items such as small Chinese OEM refrigerators and blenders resonate with Africa’s broadly defined middle class and are supported by distributors, service centers, repair networks, and secondary spare-parts markets.

Expanding assortment remains a leading growth driver. Gross items sold from international sellers grew 82% year-over-year, reflecting deeper engagement with cross-border supply and broader category availability. During Q&A on the conference call, Dufay ranked the drivers as 1) assortment, 2) market coverage, 3) marketing, and 4) improvement in quality and satisfaction. Marketing ramped in Q3 and Q4, but it builds on structural improvements in product breadth and geographic reach.

Order economics also remain a focus. Repurchase rates improved by 422 basis points year-over-year, reinforcing that customer engagement is strengthening alongside volume growth. Jumia conducted a cohort analysis concluding that “46% of new customers, who placed their first order in the third quarter of 2025, made a second purchase within 90 days, compared to 42% of new customers in the third quarter of 2024.” The company’s stickier and higher quality customer base supports growth and makes the operating leverage even more profitable.

Jumia continues to optimize for lower out-of-stock rates and higher delivery success. Prepayment is a meaningful lever in this effort. As Dufay noted, “the success rate for prepaid orders is close to 100%.” Increasing prepaid penetration directly improves fulfillment economics and contributes to margin stability.

The Macro Backdrop and Competition

Macro conditions appear more stable entering 2026. In our discussion, Dufay remarked, “I cannot ask for better news on the macro side.” On the conference call, he added, “We are turning cautiously optimistic on the macro side. FX rates have been stable or slightly improving. Importers can import again.” Nigeria was cited as an example of economic reforms gaining traction, and Egypt’s recovery reinforces the view of a stabilizing macro backdrop.

Competitive intensity has moderated as well. Competition from Chinese exporters has become “less intense,” and Dufay noted on the conference call that pressure has slightly decreased over the past two to three quarters. Regulatory scrutiny of international platforms not contributing meaningfully to local economies has increased. Still, he emphasized that a further pullback by competitors would not be an “absolute game changer.” Execution remains central.

Advertising Revenue

Advertising revenue reached $2.9M in Q4, up 42% year-over-year, but remains around 1% of GMV. Dufay acknowledged on the conference call that “2025 was disappointing” for advertising revenue due to disruption from the rollout of a new retail advertising tool. Vendor feedback has improved, and while advertising revenue may eventually approach 2% of GMV, that is not expected in 2026.

Capital Discipline

Capital discipline remains a clear priority. On the conference call, Dufay stated, “While we may continue to look opportunistically at financing options, based on our current trajectory, we continue to believe our existing liquidity is sufficient to reach profitability without raising additional capital.” In our discussion, he clarified that “we are not chasing options.” Opportunistic financing would only be considered under highly favorable circumstances. The company’s objective is to avoid ever being in a position where capital must be raised out of necessity. Jumia ended Q4 with $77.8M in liquidity and a Q4 cash burn of $4.7M versus $30.6M in Q4 2024, providing more evidence of capital discipline and an improving balance sheet.

Short-Term Disappointment

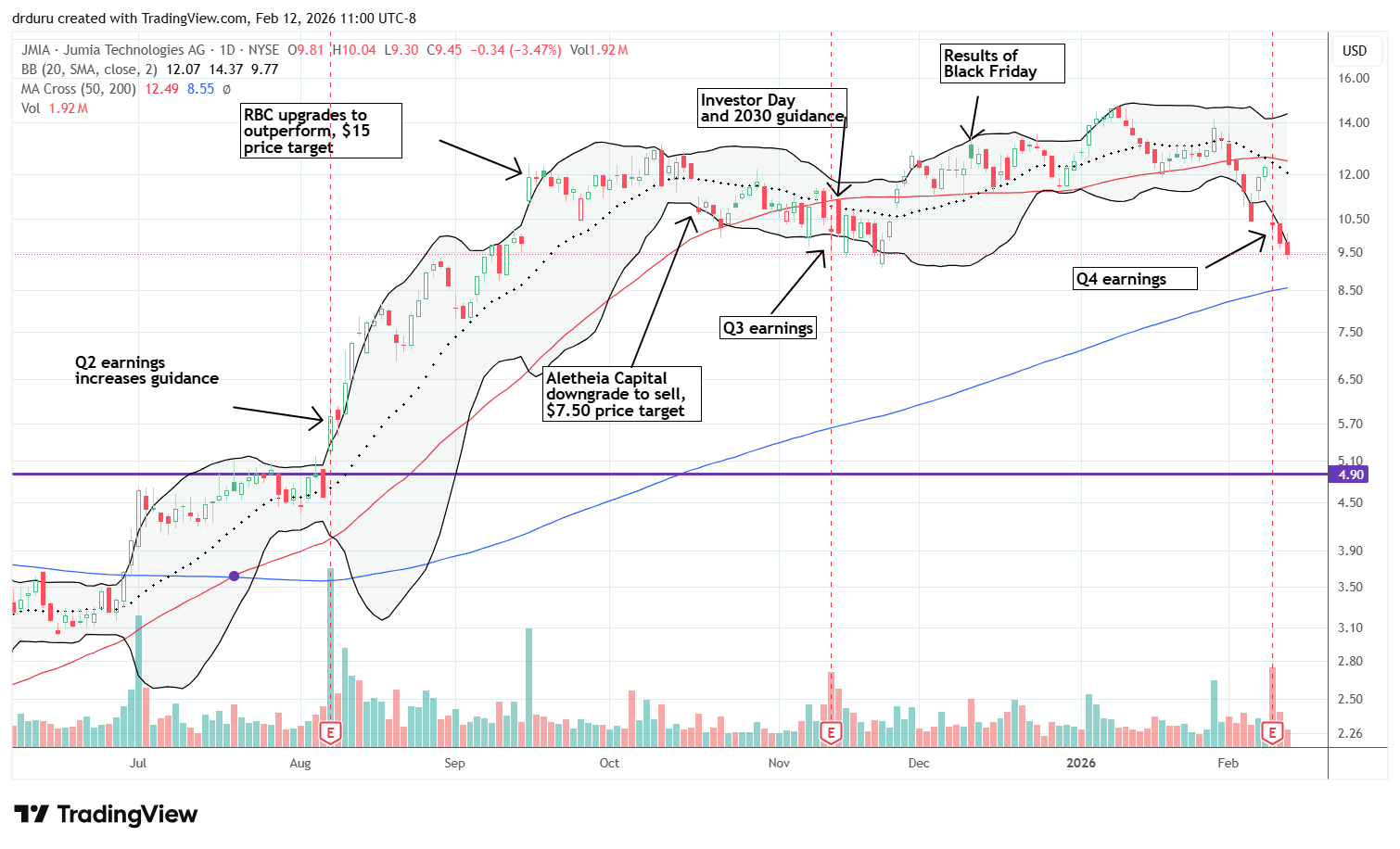

Despite the company’s operational achievements, the market reacted negatively to JMIA. The GMV guidance likely caused this latest bout of short-term disappointment. The stock gapped down from resistance at its 50-day moving average (DMA) (the red line in the chart below) for a 15.8% loss, followed by another 5.2% decline. I added shares on both days with a focus on continued directional momentum and evidence that the company’s enduring strategy continues to win. I will add shares again on a test of 200DMA support (the blue line) around $8.75 if sellers push the stock that far. Note that at the time of writing JMIA trades below its price after the stellar Black Friday results, reassuring 3 earnings, and a compelling Investor Day and 2030 guidance.

Conclusion

Q4 2025 showed scale expanding margins, fulfillment costs declining, infrastructure supporting higher volumes, macro conditions stabilizing, and a balance sheet not dependent on new capital. As Dufay summarized, “We believe we are in the right markets, at the right time, and finally with the right product-market fit.”

The ramp to 2030 remains intact, and I will continue to invest in JMIA accordingly.

Be careful out there!

Full disclosure: long JMIA