“Historically low levels of interest rates globally and the current backdrop of low volatility across financial markets may encourage market participants to underestimate the likelihood and severity of tail risks. There are increasing signs that investors, in searching for yield, may be increasing the vulnerability of the financial system to shocks. This vulnerability is amplified by structural changes in markets potentially reducing the availability of market liquidity at times of stress.” – Financial Stability Report, June 2014 | Issue No. 35, The Bank of England

It took me a few weeks to get around to listening to the press conference for the Bank of England’s (BoE) latest Financial Stability report, but it proved to be well worth the time and effort. Most of it was about the UK housing market and the efforts of the BoE’s Financial Policy Committee (FPC) to prevent the United Kingdom’s market from getting over-leveraged and over-heated. The FPC’s bottom-line on its regulatory measures is that the housing market is healthy now, but the FPC is looking down the road to prevent risks to financial stability:

“The recovery in the UK housing market has been associated with a marked rise in the share of mortgages extended at high loan to income multiples. At higher levels of indebtedness, households are more likely to encounter payment difficulties in the face of shocks to income and interest rates. This could pose direct risks to the resilience of the UK banking system, and indirect risks via its impact on economic stability…

{snip}

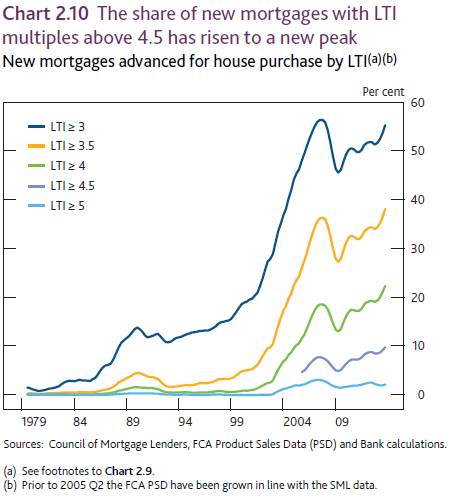

New mortgages advanced for house purchase by loan-to-income ratio

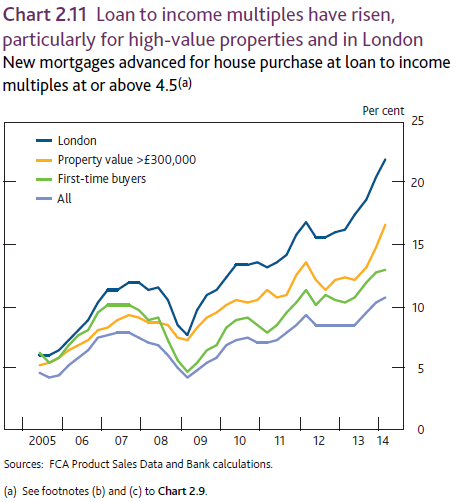

New mortgages advanced for house purchase at loan to income ratios at or above 4.5 Source: Bank of England Financial Stability Report for June, 2014

Reporters attending the press conference were right to question the efficacy of financial measures which will supposedly not impact the health of the housing recovery. {snip}

The FPC’s ultimate conclusion is important:

“Liquidity risk premia vary significantly throughout the economic cycle, rising sharply during periods of stress. That was demonstrated during the financial crisis, with indicators of liquidity risk premia rising abruptly in 2008–09. Since then, they have fallen close to their pre-crisis levels and, amid increasing signs of investors searching for yield, appear slightly below average in some fixed-income markets.

But this is not necessarily a benign signal. There is a risk that current valuations are masking an underlying fragility, particularly in the light of a post-crisis reduction in banks’ market-making and proprietary trading activity. As discussed in Section 2, this fragility could be exposed if investors simultaneously sought to unwind their fixed-income positions in response to a common interest rate or volatility shock, causing secondary market liquidity to dry up in pockets of the financial system. Such a sell-off could result in wider financial market disruption.” (Section 2 is a discussion of short-term risks to financial stability).

MY conclusion from this statement is that the FPC is announcing that the market IS under-pricing very real fragilities in the financial system. {snip}