(This is an excerpt from an article I originally published on Seeking Alpha on January 27, 2014. Click here to read the entire piece.)

“Escape velocity won’t come cheap.” – Mark Carney, Governor of the Bank of England (BoE), January 24, 2014

This was Governor Carney’s warning to the audience at the Davos CBI British Business Leaders Lunch. It was a reference near the end of his speech summing up the prospect of maintaining low interest rates for an unusually extended period of time in order to generate a sustainable economic recovery. {snip}

Technically, there is no need to change guidance given the BoE’s current guidance does not promise action. In fact, if anything, it promises that the BoE reserves the right to inaction no matter what happens with unemployment. I suspect this announcement is more about redrawing the line in the sand to further delay the day of reckoning when reporters at BoE press conferences pepper Carney and his colleagues with demands for a specific timetable for rate hikes. {snip}

The on-going question for Carney, the BoE, and economists is the “surprisingly poor performance” of the supply side of the economy, its production capacity. {snip}

Carney also made a point to cite the currency as one of the factors suddenly keeping inflation in check (emphasis mine):

{snip}

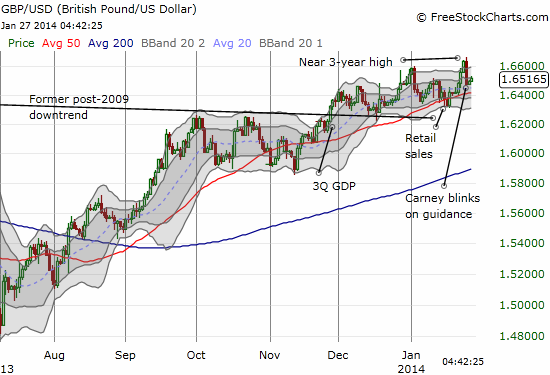

I am sure this kind of commentary heightened the sense that the Bank of England is finally getting uncomfortable with the steady strengthening in the British pound (FXB). {snip}

Source: FreeStockCharts.com

I think this dip represents a fresh trading opportunity to go long the pound. {snip}

Developing an upside target for the pound is difficult given its dependence on developments in the eurozone. {snip}

Be careful out there!

(This is an excerpt from an article I originally published on Seeking Alpha on January 27, 2014. Click here to read the entire piece.)

Full disclosure: long USD/GBP