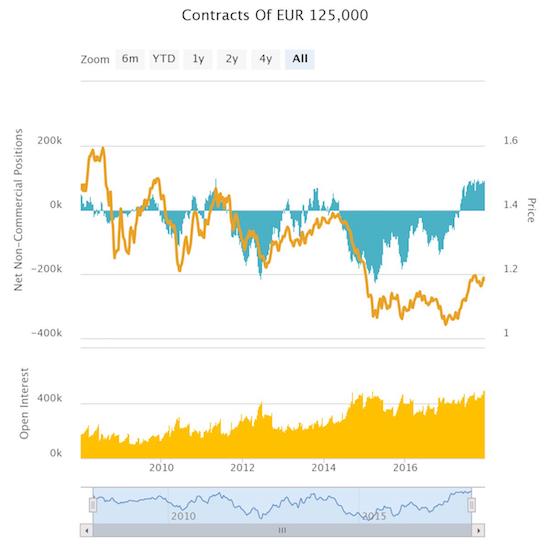

Speculators have not been this bullish on the euro since at least 2008.

Source: Oanda’s CFTC’s Commitments of Traders

These charts reveal a distinct sentiment shift on the euro this year. Since 2008, speculators spent the majority of the time as firm euro bears. The new high in net long positioning going into 2018 signals strong odds for fresh momentum for the euro.

Right now, EUR/USD is pivoting around its 50-day moving average (DMA) after leaving behind a near 4-year high in September. EUR/GBP flirts with a major breakdown as it churns below converged 50 and 200DMA resistance.

Source: FreeStockCharts.com

The speculative breakout in the euro came ahead of the Thursday, December 14 meeting of the European Central Bank (ECB). The euro rallied going into the meeting and sold off after the meeting and into the end of the week. I think the selling was overdone; likely a reaction to the ECB sticking to its plans for monetary policy with a general lack of strengthening in the inflation outlook. In particular, ECB President Mario Draghi reiterated that the bond purchase timeline remained open-ended. Still, I was encouraged by the ECB’s increasing bullishness on the economy. The ECB even raised its growth forecasts and noted the strengthening of the economic expansion. From the transcript (emphasis mine):

“The latest data and survey results point to solid and broad-based growth momentum…

This assessment is broadly reflected in the December 2017 Eurosystem staff macroeconomic projections for the euro area. These projections foresee annual real GDP increasing by 2.4% in 2017, 2.3% in 2018, 1.9% in 2019 and 1.7% in 2020. Compared with the September 2017 ECB staff macroeconomic projections, the outlook for real GDP growth has been revised up substantially.”

During the Q&A, Draghi reiterated and repeated the ECB’s confidence:

“…by and large the overall discussion today reflected the increasing confidence that we have in the convergence of inflation towards a self-sustained inflation path in the medium term and towards our objective. Generally speaking, the growth news is very positive…

The developments that we are witnessing in the real economy certainly increase our confidence for an output gap that will get closed in the course of the next year and improving conditions in the labour markets, which in due time should increase pressure on nominal wages. As you know, that has been one of the variables we’ve been looking more at as one of the drivers of the underlying inflation and therefore one of the drivers for a sustained progress in headline inflation.”

On balance, these observations would make me expect a strong rally in the euro in response. However, Draghi made an oblique reference to undesirable strength in the euro as a risk factor for monetary policy: “…downside risks continue to relate primarily to global factors and developments in foreign exchange markets.” In other words, a strengthening euro will apply further downside pressure on inflation and likely dissuade the ECB from even contemplating monetary tightening in response to the improving economic outlook. On the other hand, low rates, low inflation, and strong economic growth are all good for stocks. Thus, the SPDR EURO STOXX 50 ETF (FEZ) may look undervalued especially given it has not printed a new post-recession high since the summer of 2014.

Source: FreeStockCharts.com

So while the action of the previous week rekindled my bullishness on the euro, I am duly noting that market trading has not yet affirm a renewed bullishness.

Be careful out there!

Full disclosure: no positions