The year 2026 is off to a fast start. After immediately testing my shopping list for the year on software stocks, and Intel Corporation (INTC), headlines from NVIDIA (NVDA) at the Las Vegas Consumer Electronics Show (CES) pressed my positioning in AI-related stocks. CEO Jensen Huang declared (emphasis mine):

“The power of Vera Rubin is twice as high as Grace Blackwell. And yet, and this is the miracle, the air that goes into it, the air flow, is about the same and very importantly, the water that goes into it is the same temperature, 45°C with 45°C, no water chillers are necessary for data centers. We’re basically cooling this super computer with hot water.”

Tuesday trading opened with a sharp selloff in stocks related to data-center cooling. At one point, one of my data-center cooling stocks wiped out the rest of my profits in the name. At its low of the day, SPX Technologies (SPXC) finished reversing its entire breakout from October. Amazingly, buyers rushed into SPXC so fast, the stock ended the day with a 1.5% gain. The chart below shows that the 50-day moving average (DMA) (the red line) held as resistance.

Relieved that SPXC survived a major test, I realized that the near indiscriminate selling set up a pairs trade opportunity: short Modine Manufacturing (MOD), preferably via put options, and long Johnson Controls (JCI). The market is correctly questioning unit-volume assumptions in cooling, but it is incorrectly applying that logic across an entire sector, conflating volume destruction with architectural and mix shifts. That confusion is where the relative-value opportunity emerges.

The Narrative Shock: From Cooling Architecture to Cooling Volume

The initial takeaway from NVIDIA’s Rubin platform was architectural rather than macroeconomic. Rubin emphasizes higher performance per watt and more efficient thermal management, including expanded use of direct liquid cooling and warmer water loops. In isolation, that suggests a shift in how cooling is delivered, not whether it is needed.

However, the market quickly extended that logic into a more aggressive chain of assumptions: higher performance per watt → fewer GPUs per workload → fewer racks → fewer cooling systems in absolute terms. That final step, an absolute reduction in cooling demand, likely drove the selling.

For example, in “Modine Manufacturing tumbles as Nvidia Rubin chip could reduce data center cooling needs” Seeking Alpha pointed out that Rubin “will likely reduce the need for cooling systems in data centers” by improving performance per watt and reducing the number of GPUs required for AI workloads.

Why Modine Became the Epicenter of the Selloff

Modine sits at the most exposed point in this narrative because its data-center thesis is explicitly volume-driven. The company “designs, engineers, and manufactures thermal solutions including air handlers, condensing units, and chillers used to cool data centers”. Its growth story depends on shipping more physical cooling equipment as AI infrastructure scales. Management directly reinforced that dependence during the October earnings call. CEO Neil Brinker said:

“I currently see a path to deliver more than 60% revenue growth in data center this year on our way to achieve over $2 billion in revenues in fiscal 2028. This year marks a period of major investment in our data center businesses, driven by strong market demand.”

That forecast implicitly assumes continued growth in rack count and cooling unit deployment. Rubin challenges that assumption at its core. If higher-performance accelerators reduce the number of GPUs (and therefore racks) needed to achieve a given compute outcome, then Modine’s unit volume becomes a pressure point. Pricing power, efficiency, or execution cannot fully offset a shrinking addressable shipment base.

With a bullish narrative instantly turning into a burden, MOD broke down its 200DMA (the blue line) at one point for a 20.6% loss. The subsequent relief rally reduced that loss to 7.5%. I bought a January $120 put option with the stock down about 9%. At the time of writing, MOD slipped right back to 200DMA support; I do not expect support to last long.

Why Johnson Controls and Trane Are Being Mispriced

The logic applied to Modine does not apply cleanly to Johnson Controls or Trane (TT), even though both sold off sharply in sympathy with MOD.

Unlike Modine, these companies are not simple proxies for cooling unit volume. Their exposure includes:

- integrated building systems

- controls and automation

- services and lifecycle management

- liquid-cooling infrastructure and distribution

- long-lived installed bases tied to uptime, redundancy, and reliability

Even if GPU efficiency improves and rack counts grow more slowly, data centers do not become simpler. Power density per rack continues to rise, reliability requirements increase, and thermal management becomes more specialized.

In practice, efficiency gains tend to reallocate spending within the stack, not eliminate it (per multiple sources that I referenced). Dollars move away from some categories and toward others: liquid distribution, controls, system integration, and services.

The selloff treated Johnson Controls and Trane as if they were indistinguishable from a unit-volume thermal OEM. They are not. I decided the technicals favored a stronger rebound in JCI than in TT. For the long side of my pairs trade I bought a January $115 call. At the time of writing, JCI faded quickly after a positive open. TT is up 0.9% after falling sharply after its open.

The Trade

I had to move fast to understand the opportunity. For example, I used ChatGPT to help me track down resources to understand the various companies caught in the selloff as well as assess my logic for establishing a pairs trade. I also decided to hold SPXC and my position in Vertiv (VRT) which helps manage power loads and consumption in data centers. In summary:

- Short Modine (MOD)

- expresses downside to a growth story tied directly to cooling unit volumes

- benefits if the market continues to pressure shipment-dependent models

- Long Johnson Controls (JCI)

- captures rebound potential as investors differentiate between volume exposure and systems exposure

- benefits if the narrative shifts from “less cooling” to “different cooling”

The market apparently is correctly re-examining linear assumptions that tie AI growth directly to ever-increasing cooling unit volumes. However, the market is likely wrong to assume that all cooling-adjacent companies share that risk equally. Modine’s selloff reflects a challenge to its volume-driven growth thesis.

Johnson Controls and Trane are collateral damage from a sector-level retrenchment.

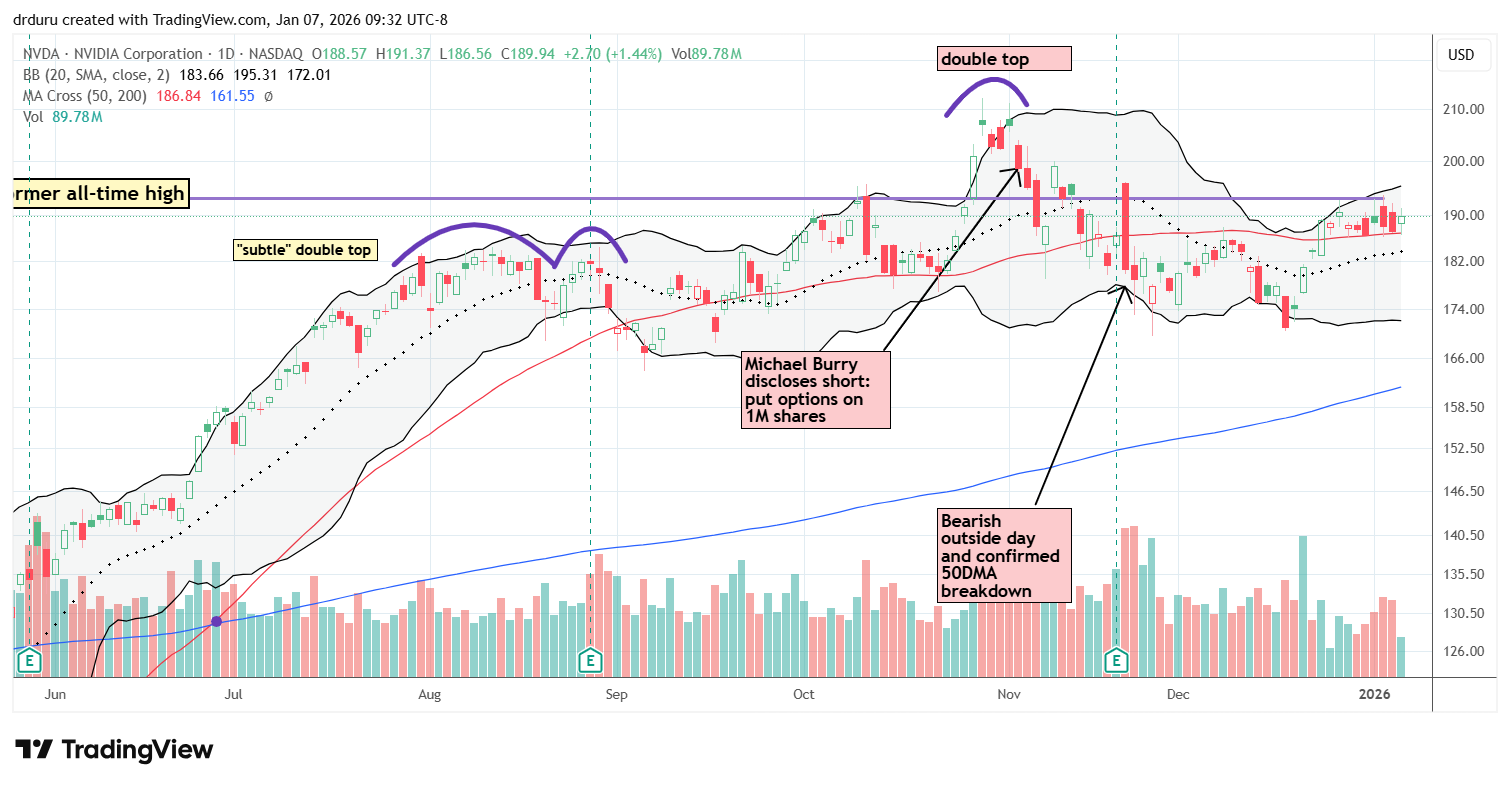

Interestingly, in the middle of all the carnage, NVDA fell 0.5% and held support at its 50DMA. The stock continues to trade just below its previous all-time high in what looks like an extended period of price consolidation.

Be careful out there!

Full disclosure: long SPXC, long VRT, long JCI call, long MOD put

This trade is moving fast. I already took profits on the MOD put. JCI is now, surprisingly, under-performing MOD. I might cycle through this pairs trade periodically.