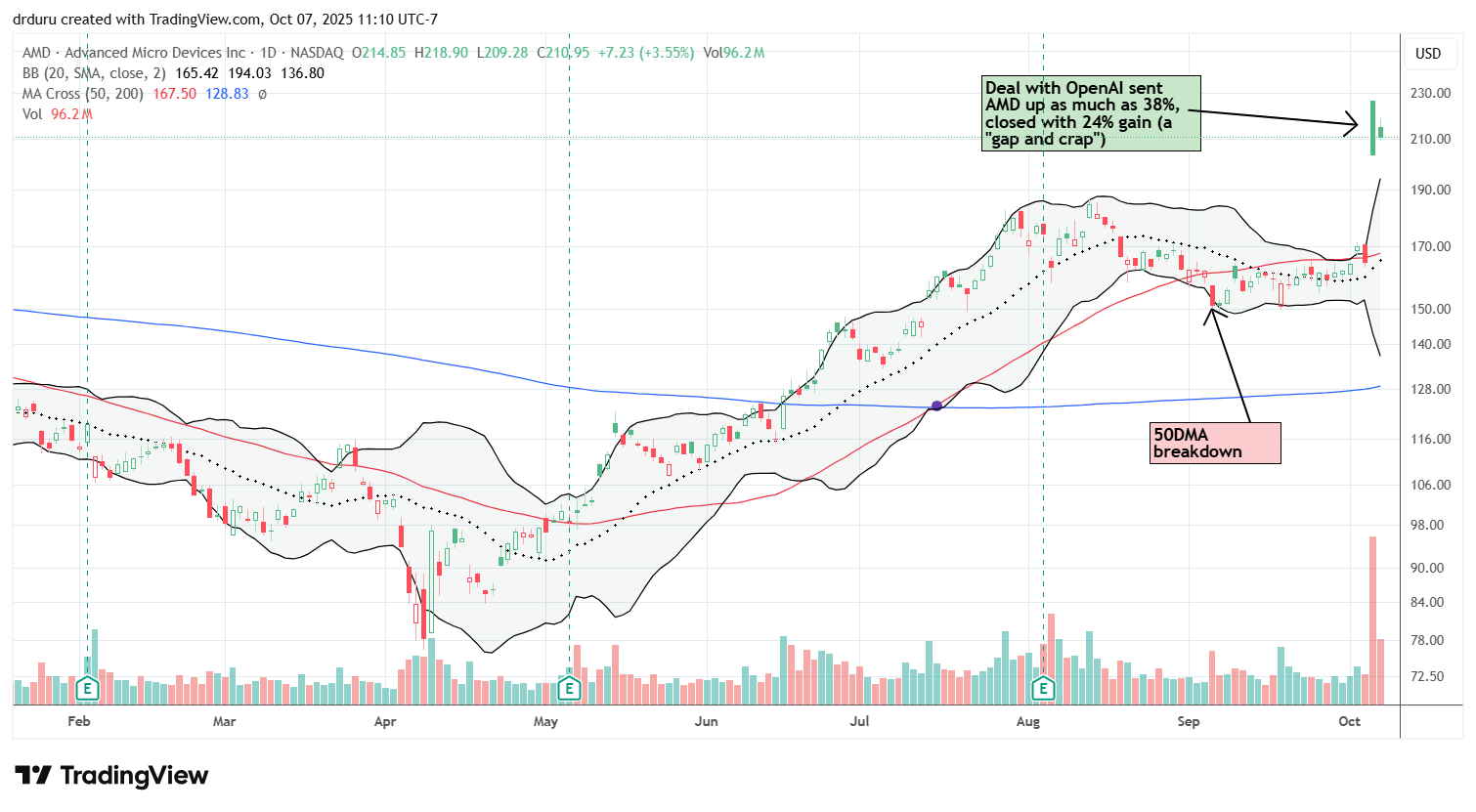

Exactly one month ago, I explained I would stick with Advanced Micro Devices (AMD) despite disappointing weakness in shares. I looked through the short-term bearish signal of a technical breakdown (below the 50-day moving average (DMA)) and pinned my expectations on AMD continuing to catchup with a red hot, AI-driven semiconductor industry. When AMD soared as much as 38% on news of a mega-deal with OpenAI, my attitude flipped 180 degrees. I suddenly looked for reasons to sell and take profits on such an extreme move. After all, with the stock market already in melt-up mode, can this sudden and abrupt euphoria hold up?

Well, I looked and looked and could not find a compelling reason to sell. The details of the deal, or the lack of details, make me wary, but the valuation metrics are not bad enough to convince me to close out. So I am left with watching the technicals for a potential sell sign.

An Amazing Deal with Caveats

AMD’s deal sounds fantastic for the company: “a 6 gigawatt agreement to power OpenAI’s next-generation AI infrastructure across multiple generations of AMD Instinct GPUs.” However, the caveats begin immediately from there. Most glaring of all is the lack of a valuation for the deal. AMD did not disclose revenue expectations or a timeline for recognizing the revenue. In fact, if I did not expect better, the deal sounded like AMD is paying OpenAI to buy its Instinct MI450 GPUs!

Rather than state a revenue gain, the deal discloses what OpenAI will earn from letting AMD supply GPUs. AMD will issue warrants on 160M shares at an exercise price of just $0.01, essentially giving away the shares which constitute about 10% of the company’s current outstanding shares. Those shares were worth $26.3B before the deal was announced and $32.6B after the deal. So does AMD expect to earn even more revenue than $30B or $40B? Who knows at this point.

Moreover, the deployment of the first gigawatt will not begin for another year or so. The deal disclosure also says nothing about the full timeline of the deployment.

My eager search for more details moved on to the 8-K SEC filing.

Giving away 10% of a company is very dilutive to existing shareholders. Sometimes companies will strike a separate hedging transaction with a financial institution to minimize the dilutive effect of warrants. This deal does not seem to carry such protections. Instead, a vesting schedule laddered by stock price targets absorbs some of the burden of the dilution. AMD’s share price must hit certain milestones before OpenAI can cash in. The warrants also have a 5-year vesting period.

The highest price target looks quite attractive to shareholders who want to hold on and see what happens. Per the SEC filing: “vesting of Warrant Shares are further subject to achievement of specified Company stock price targets that escalate to $600 per share for the final tranche and stock performance thresholds. Additionally, each tranche of vested Warrant Shares is subject to the fulfillment of certain other technical and commercial conditions prior to exercise.” The final threshold of $600 represents a near triple from today’s stock price!

This astronomical threshold contains a message for the market. OpenAI and AMD expect this partnership to be so valuable that AMD will soar in value. Thus, this partnership must generate significant revenue for AMD. Hopefully AMD will disclose the exact scale of the expected revenues in coming earnings reports.

The Valuation

I next looked at valuation to find a reason to justify selling AMD. After all, even with all the excitement about the deal, AMD is “only” trading around its all-time high set last year (closing all-time high of $211.28, intraday all-time high at $227.30). While the valuation makes me wary, I could not quite bring myself to sell.

Seeking Alpha grades AMD’s valuation at a bottom of the barrel D+ given the stock trades well above sector medians across a range of valuation metrics. AMD has a non-GAAP 59 price/earnings and 122 GAAP price/earnings. Fortunately, earnings growth estimates are quite generous: 18% for 2025, 57% for 2026, 32% for 2027, and 44% for 2028. Thus, the P/E to growth (PEG) ratio is high but not “run for the hills” high. AMD shares could consolidate from here as the stock “digests” its valuation.

As a hardware company, AMD has a very high price/sales ratio of 11 and forward price/sales of 10. At least this valuation is less than half of Nvidia’s (NVDA). Seeking Alpha gives NVDA’s valuation an outright F grade.

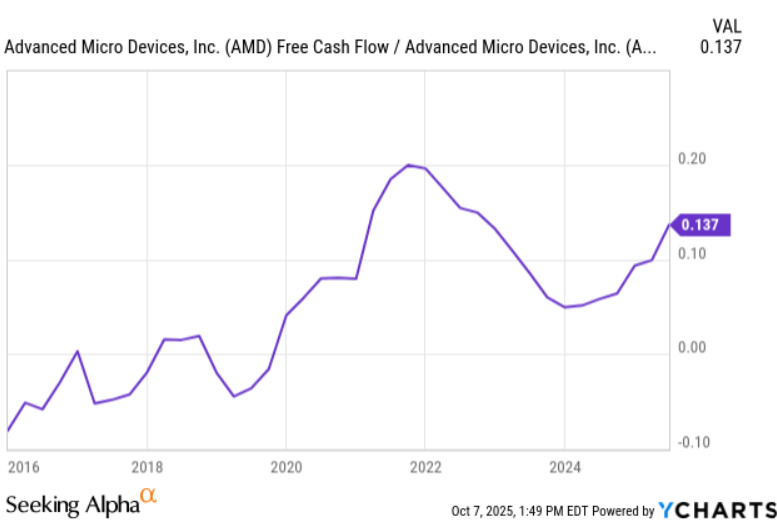

Finally, AMD’s cash flow margin remains favorable and is still recovering from a 2024 trough. I have recently adopted the habit of checking cash flow margin as a way to assess a company’s ability to sustain its valuation, no matter what the market is paying.

Clinging to the Technicals

I last turned to the technicals to inform my sell or hold decision. I remain wary, so the message of the market might be my final judge. At the time of writing AMD managed to gap up a little higher thanks to analyst action.

Jefferies, probably reluctantly, got off the fence and upgraded AMD from a hold to a buy with a $300 price target. Somehow, Jeffries estimates “the partnership has the potential to generate well over $100B from OpenAI, new, and existing customers over the next four years…The announcement of OpenAI as a lead customer with the potential for $80-100B in revenue across 6GW of compute through 2030 materially changes that outlook.” The resulting gap higher now gives me a clear stopping out point: below the low of “deal day” at $203.35. If I get stopped out, I am fine waiting to buy back into AMD at lower prices OR in the very bullish case, buying a breakout above the highs of deal day at $227.

This second day of gains is important because AMD printed a “gap and crap” in response to the deal: the shares open at its high of the day and close at a much lower price. Such reversals typically lead to lower prices in the short-term, especially following big news. Essentially, a gap and crap indicates an exhaustion of the most motivated buyers.

Oracle (ORCL) is a recent, and even historic, example of the importance of buyer exhaustion. I covered the ORCL trade in the wake of its own big OpenAI deal (anyone worried yet that OpenAI is at the center of so many blockbuster AI deals?). While ORCL avoided the dreaded gap and crap on the first day of post-earnings trading. The sellers showed up the next day in force. A subsequent rebound failed in picture-perfect form right at the all-time high set by earnings.

Technicals matter. The technicals will guide my short-term sell or hold decision. If I sell, I will closely monitor AMD for the next buying opportunities.

Be careful out there!

Full disclosure: long AMD, long ORCL call spread

My habit, when it seems to me the market is over-valuing a stock I own, is to sell “some”: optimally, a fraction that takes out my original investment so the rest is “house money”.

That’s a great strategy. In this case, my profit is not yet big enough to make it worth trimming to house money size. But at least analysts keep rushing to upgrade their hold ratings! 🙂

Unfortunately, I sold my $AMD shares today and locked in remaining profits. The stock broke down below its 50-day moving average and kept going. The momentum as completely turned against the stock, and the bad reaction to $NVDA earnings helped grease the slide. I have two re-entry points. On the downside, $150 to $185. That’s the continued sell-=off scenario. On the upside, $220. That’s the quick recovery scenario.