About six weeks have passed since Apple printed an apparent bottom in the wake of the tumultuous trading surrounding its April earnings report. With the benefit of hindsight, I think it is worthwhile to look back at some important highlights to consider whether this bottom is a sustainable one and what the prospects might be for further upside in the near-term.

One of the most intriguing patterns that emerged in Apple’s trading was the tight correlation between the put/call open interest ratio and AAPL’s stock price. Apple’s post-earnings recovery peaked as soon as that put/call ratio peaked. (Apple reported earnings on April 23rd. I discussed the pre-earnings trade in “Bullish Earnings Trading Patterns And Sentiment Collide With Apple’s Recent Downtrend.” That post also updated the charts showing Apple’s daily trading patterns).

Source: Schaeffer’s Investment Research, Apple put/call open interest ratio

The window of opportunity to take advantage of a pattern is sometimes short. Yet, often one pattern gives way to a new one. Notice that in mid-May, two weeks after Apple’s post-earnings price recovery ended, the correlation completely reversed. NOW, the put/call ratio continues to decline, but AAPL is gradually increasing. The ratio has gone from a contrarian indicator to a supportive one.

It turns out that mid-May was an important turning point in the stock that I think confirms a sustained bottom. At the end of April, Russia’s richest man, Anisher Usmanov, announced that he had invested $100M in Apple to take advantage of its low valuation. Two weeks later, several hedge funds announced major changes in their Apple holdings as of the end of the first quarter (percentages represent net change in shares):

- David Tepper’s Appaloosa Management: -40%

- Julian Robertson’s Tiger Management: -100% (sold entire position)

- Tiger Global: -75%

- Blue Ridge Capital: -100%

- David Einhorn’s Greenlight Capital: +83.5%

- Maverick Capital: +26.7%

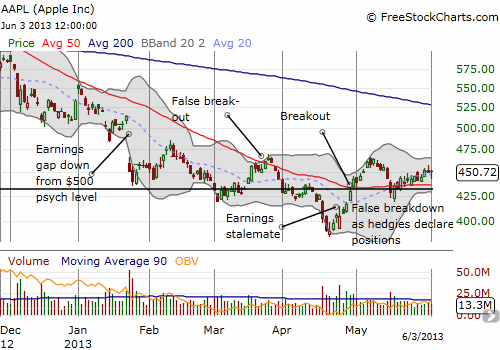

The net-net of all these disclosures was a seemingly ominous 3.4% plunge on high selling volume that took AAPL through its 50-day moving average (DMA).

Instead of follow-through selling, AAPL rallied the very next day and two days later recovered all its losses. The stock has slowly but surely inched its way higher ever since. During this period, CEO Tim Cook also delivered an excellent performance discussing Apple’s management of taxes with the U.S. Senate’s Permanent Subcommittee on Investigations that included a compelling case for corporate tax reform. I think these actions increase the odds that a major overhang of sellers has passed through the system and that the major buyers have moved into a position of support.

Source: FreeStockCharts.com

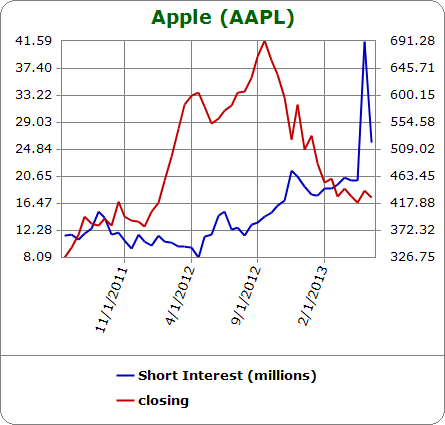

Something else important happened in mid-May that may have helped this fresh turn-around: short interest took a tremendous tumble.

Starting in early April, shares short in AAPL rose from a low around 8M to 21M by year-end. It held in a tight range until the April earnings. While we only have the settlement date of May 1st to work with, I strongly suspect shares short shot skyward BEFORE earnings. On May 1st, shares short were a whopping 41.6M shares. Two weeks later, mid-May (May 15th), shares short dropped back to 26.0M shares. This represents 2.8% of AAPL’s float. This short interest is a small fraction, but the sharp and abrupt changes matter for flashing a likely positive change in sentiment and a final relief of whatever selling pressure came with the increased interest in shorting the stock. Moreover, the amount of money involved on an absolute basis is incredible. At today’s price, the shares short are worth about $11.7 BILLION. That is a LOT of money betting against a stock! Here are the data graphically, again from Schaeffer’s:

Source: Schaeffer’s Investment Research, Short Interest

Note that it is also very possible that some portion of the increase in shares short came from institutions looking to hedge some of the $17B in Apple corporate bonds that were bought at the end of April. If so, then shares short should not decrease much further from current levels.

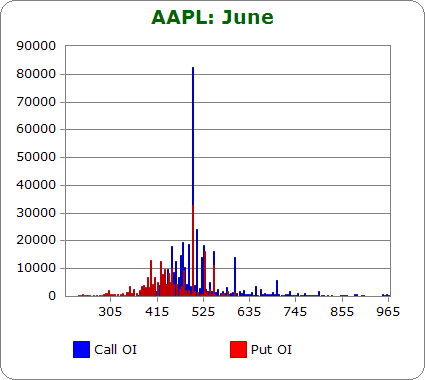

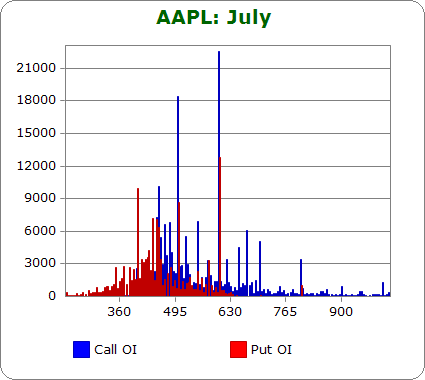

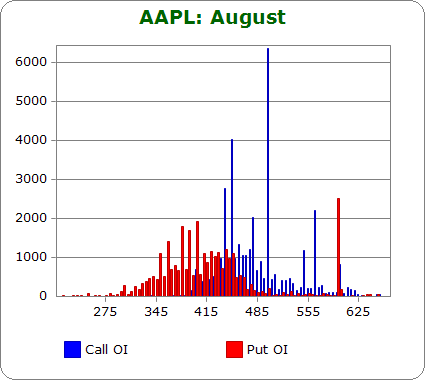

So far, so good. It seems AAPL can sustain a bottom. However, it seems for most of the summer, AAPL is also highly unlikely to surpass the $500 mark. Such an achievement would finally fill most of the large January post-earnings gap down. Apple’s option open interest includes what is essentially a brick wall of calls at the $500 strike. In June, July, and August, the open interest on calls at the $500 strike far surpasses almost all other open interest, calls and puts. In July, an even larger swell exists at the $600 strike; these options are essentially now worthless (and expire BEFORE July earnings on the 23rd).

A large swell of open interest is important because of the amount of money at stake. For example, market makers have a substantial interest in seeing Apple remain below $500 to maximize profits. I also suspect that some Apple holders have sold covered calls at $500 (particularly for July expiration) with the assumption that the stock would not overcome that level anytime soon. I post below the open interest configurations for June, July, and August from Schaeffer’s. Each chart is followed by the timeline of open interest using data from Etrade.com. (I have positioned the cursor in each timeline where the largest jump in open interest seems to happen).

Note that in each configuration, the dominance of the $500 calls sticks out like it beckons for attention. Time is running out for the June and July $500 holders as prices have eroded significantly from much higher levels months ago. The August holders are likely helped by higher implied volatility from July earnings. As those earnings approach, $500 should become a major focal point of resistance for Apple’s stock, like a hard stop. On a valuation basis, AAPL would still only hold a 12 trailing and forward P/E at $500, so it is reasonable to expect that speculators could continue to pile into the $500 call strikes, adding to the likely resistance at that level.

AAPL gained 10% in 10 calendar days after April earnings and almost another 10% in another 9 days to the most recent peak, so it is certainly possible that AAPL can gain a lot of ground in a hurry. However, I would be highly surprised to see AAPL closing in on $500 by June expiration. A run to $500 for July expiration is much more intriguing given the proximity to earnings and the possibility of a roundtrip from January earnings. Traders insisting on playing such a run may be better served by a call spread like 490/500 ($490 long, $500 short). Assuming Apple will hit a brick wall near or at $500, the call spread cuts the cost of the trade roughly in half while giving up almost none of the potential upside around the time of expiration.

This analysis benefited from hindsight and took a snapshot of the current trading behavior. In the coming weeks, it will be important to watch how these scenarios change and to adjust if necessary. Apple’s bias finally seems bullish now with major selling and sentiment overhang removed and major buyers firmly in place. If the bullish momentum increases, it will next become important to watch for excesses that could slow the stock down again; for example, a surge in open interest at lower strikes and/or a put/call ratio drops much lower than current levels around the 25 percentile ranked over the last one to two years. The stock gets the “benefit of the doubt” on dips unless it breaks that major mid-May turning point.

Be careful out there!

Full disclosure: long AAPL shares and calls